What is the Go Direct FHA 100 mortgage financing?

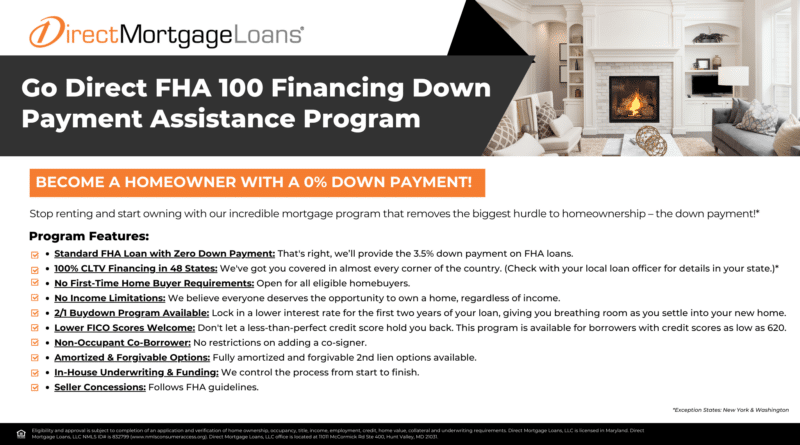

The Go Direct FHA 100 Mortgage Financing program is a home loan solution offered by Direct Mortgage Loans allowing qualified buyers to finance 100% of their home purchase. This means no traditional down payment is required for the home purchase. Built on the foundation of a standard FHA loan, this program adds a second lien to cover the required 3.5% down payment, giving buyers an opportunity to purchase a home with little to no upfront cash.

This program was designed for individuals who meet FHA loan requirements but are held back by the upfront costs typically associated with buying a home. With Go Direct FHA 100, more borrowers can take confident steps toward homeownership without draining their savings.

Key Features Of The Go Direct FHA 100 Loan

The Go Direct FHA 100 loan stands out with features aimed at improving accessibility and affordability:

- 0% Down Payment: Unlike most traditional loans that require upfront cash, this program allows buyers to finance the entire purchase price. The 3.5% down payment typically required by FHA is covered by a second lien, removing one of the biggest barriers to homeownership.

- Standard FHA Guidelines: Benefit from predictable and flexible underwriting of FHA loans. This includes accommodating credit score requirements and allowing higher debt-to-income ratios than many conventional loans.

- Second Lien Financing: The standard second-lien option is a 10-year amortizing loan with monthly payments. A separate forgivable option may be available in limited qualifying circumstances. Terms vary by borrower and program availability.

- Potential Closing Cost Support: In some cases, the program may include options to help with closing costs, further reducing the amount of money a borrower needs at the time of purchase. This can make a significant difference, especially for buyers on a tight budget.

- Primary Residence Only: This loan must be used to purchase a home you will live in as your primary residence. It cannot be used for investment properties or vacation homes.

These features make the Go Direct FHA 100 loan a unique option for eligible buyers looking to minimize upfront costs.

Who can benefit most from the Go Direct FHA 100 Loan?

The Go Direct FHA 100 loan program is designed to support buyers who are financially stable but may not have the means to save for a large down payment. Ideal candidates include:

- First-Time Homebuyers who are entering the market and want to conserve cash for moving costs, home furnishings, or emergency savings rather than depleting reserves on a down payment.

- Renters with Steady Income who are financially responsible and ready for homeownership but haven’t been able to set aside a large lump sum for upfront costs.

- Buyers Who Qualify for FHA Loans but are blocked by the traditional 3.5% down payment requirement and would benefit from a program that helps bridge that gap.

- Younger Buyers or Recent Graduates who are new to the workforce and haven’t had time to build up savings but meet credit and income requirements.

- Families Looking to Transition from Renting to Owning who need a more accessible path to secure long-term stability and build equity over time.

The Go Direct FHA 100 loan opens the door to homeownership for many who may have assumed it was out of reach, offering a strategy to move forward in the home ownership journey without the financial strain of a large upfront investment.

How does the Go Direct FHA 100 mortgage financing work?

This program works by combining two components into one streamlined solution:

- The first mortgage is a traditional FHA loan that finances up to 96.5% of the home’s purchase price. It follows all FHA standards, including credit, income, and property requirements.

- The second lien is what makes this program truly unique. It covers the 3.5% down payment typically required by FHA, allowing the buyer to access full 100% financing.

The second lien is a key component of the Go Direct FHA 100 program and is structured as a 10-year amortizing loan. This means borrowers begin making payments on the second lien immediately as part of their monthly mortgage obligation. While Direct Mortgage Loans does offer a forgivable option, it is less commonly used in the current market due to higher interest rates. However, it remains available in certain qualifying scenarios where it may be a better fit for the borrower.

Because of this two-part structure, borrowers are often able to purchase a home with little to no cash needed at closing. This makes the Go Direct FHA 100 an excellent option for buyers who are financially ready to handle a mortgage but haven’t been able to save a large down payment.

How To Qualify For The Go Direct FHA 100 Mortgage Financing

In addition to meeting basic FHA requirements, several other financial strengths could help offset a lower credit score or borderline eligibility. Factors such as a strong employment history, a low debt-to-income ratio, a consistent on-time payment history, and having cash reserves, could all play a role in helping you qualify. These compensating factors show lenders you’re financially responsible and prepared for the commitment of homeownership.

To qualify, borrowers must meet both FHA requirements and the criteria for the second lien assistance:

- Credit Score: FHA loans generally require a minimum credit score of 580. However, borrowers with lower scores may still qualify if they can demonstrate strong compensating factors.

- Income Verification: Proof of consistent and stable income is essential. Lenders will evaluate pay stubs, tax returns, and employment history to ensure reliability.

- Debt-to-Income Ratio: Your monthly debt payments compared to your income must fall within acceptable FHA limits—typically around 43%, although this can be higher with other strengths in your application.

- Primary Residence: The property must be used as your main residence, not a secondary home or investment property.

Talking to an expert loan officer will allow you to understand your eligibility for this specific program.

How To Get The Go Direct FHA 100 Mortgage Financing

Getting started with this program is simple when working with a team like Direct Mortgage Loans. Direct Mortgage Loans’(DML’s) experienced loan officers provide step-by-step guidance throughout the process, from determining whether the FHA 100 program is a good fit, to navigating the specifics of the second lien structure. DML Loan Officers help ensure borrowers understand their financing options and feel confident through each stage of the homebuying journey. The process is designed to be smooth, transparent, and tailored to the borrower’s unique financial situation.

- Connect with one of our loan officers at Direct Mortgage Loans to discuss your goals and eligibility. A loan officer will take the time to understand your financial situation, explain how the FHA 100 program works, and assess whether you meet the qualifications. They’ll walk you through the documentation needed, help you prepare for preapproval, and outline the next steps so you can move forward with clarity and confidence.

- Get pre-approved to determine your budget and verify qualification. This step involves a thorough review of your income, assets, credit score, and debt-to-income ratio to confirm how much you can afford to borrow. Preapproval gives you a clearer picture of your price range and shows sellers that you’re a serious buyer, which could strengthen your position when making an offer on a home.

- Review your loan options, including the FHA 100 program details and second lien terms. During this stage, your loan officer will walk you through all available mortgage solutions to ensure the FHA 100 program is the best fit for your financial goals. This includes reviewing the benefits and structure of the second lien, comparing monthly payments, and discussing how this program stacks up against other FHA or conventional options. It’s a great opportunity to ask questions and make sure you fully understand your financing strategy before moving forward.

- Go house hunting with confidence, knowing you’re fully financed. Having your financing secured through the Go Direct FHA 100 program gives you a competitive edge in the homebuying process. With 100% financing in place, you can make strong offers, move quickly on listings, and avoid the delays or hesitations that come with needing to gather funds for a down payment. This added peace of mind allows you to focus on finding the right home without the financial pressure that many buyers face.

- Close on Your Home, often with minimal out-of-pocket costs. Once you’ve completed the necessary steps, reviewed your loan terms, and found your ideal property, you’ll move into the closing phase. Thanks to the Go Direct FHA 100 program, buyers frequently enter this stage with far fewer upfront expenses than traditional mortgage routes. The combination of 100% financing and potential closing cost support means that many borrowers bring very little cash to the closing table, helping reduce financial stress and make the transition to homeownership more seamless.

Our loan officers will guide you through each step, making the process as smooth and transparent as possible.

Go Direct FHA 100 Mortgage Financing FAQ’s

What makes the Go Direct FHA 100 different from a regular FHA loan?

The primary difference is how the down payment is handled. A standard FHA loan requires a 3.5% down payment from the borrower, which could be a barrier for those without savings. With the Go Direct FHA 100, the 3.5% down payment is covered by a second lien, effectively eliminating the need for a traditional down payment at the time of purchase. This unique structure allows buyers to access 100% financing while still benefiting from FHA loan terms.

Do I need to be a first time homebuyer to use the Go Direct FHA 100 loan?

No, you do not need to be a first-time homebuyer. This program is available to any qualified borrower who meets the FHA loan requirements and is purchasing a primary residence. However, the structure of the program makes it especially attractive for first-time buyers who may not have equity from a previous home to apply toward a down payment.

Are there income limits to qualify for the Go Direct FHA 100 loan?

There are no set income limits tied specifically to this program. Instead, qualification is based on your ability to repay the loan, which includes reviewing your employment, income stability, and debt-to-income ratio. This flexibility allows a broader range of borrowers to take advantage of the program, regardless of whether their income falls within a specific bracket.

Can the Go Direct FHA 100 be used to purchase any type of property?

The property must meet standard FHA guidelines. This typically includes single-family homes, townhouses, and 1-4 unit properties, as long as one unit is owner-occupied. Manufactured homes may also be eligible if they meet FHA property standards. The property must serve as your primary residence, so vacation homes or investment properties are not eligible under this program.

Eligibility and approval is subject to completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral and underwriting requirements. Direct Mortgage Loans, LLC NMLS ID# is 832799 (www.nmlsconsumeraccess.com). Direct Mortgage Loans, LLC office is located at 11011 McCormick Rd Ste 400, Hunt Valley, MD 21031.