Discover Home Equity Loans

If you want to convert the equity in your home into cash, you might want to consider a home equity loan. Read on to find out how a home equity loan works, the different types available, as well as the pros and cons. This will help you determine if this loan option is right for you.

What is a Home Equity Loan?

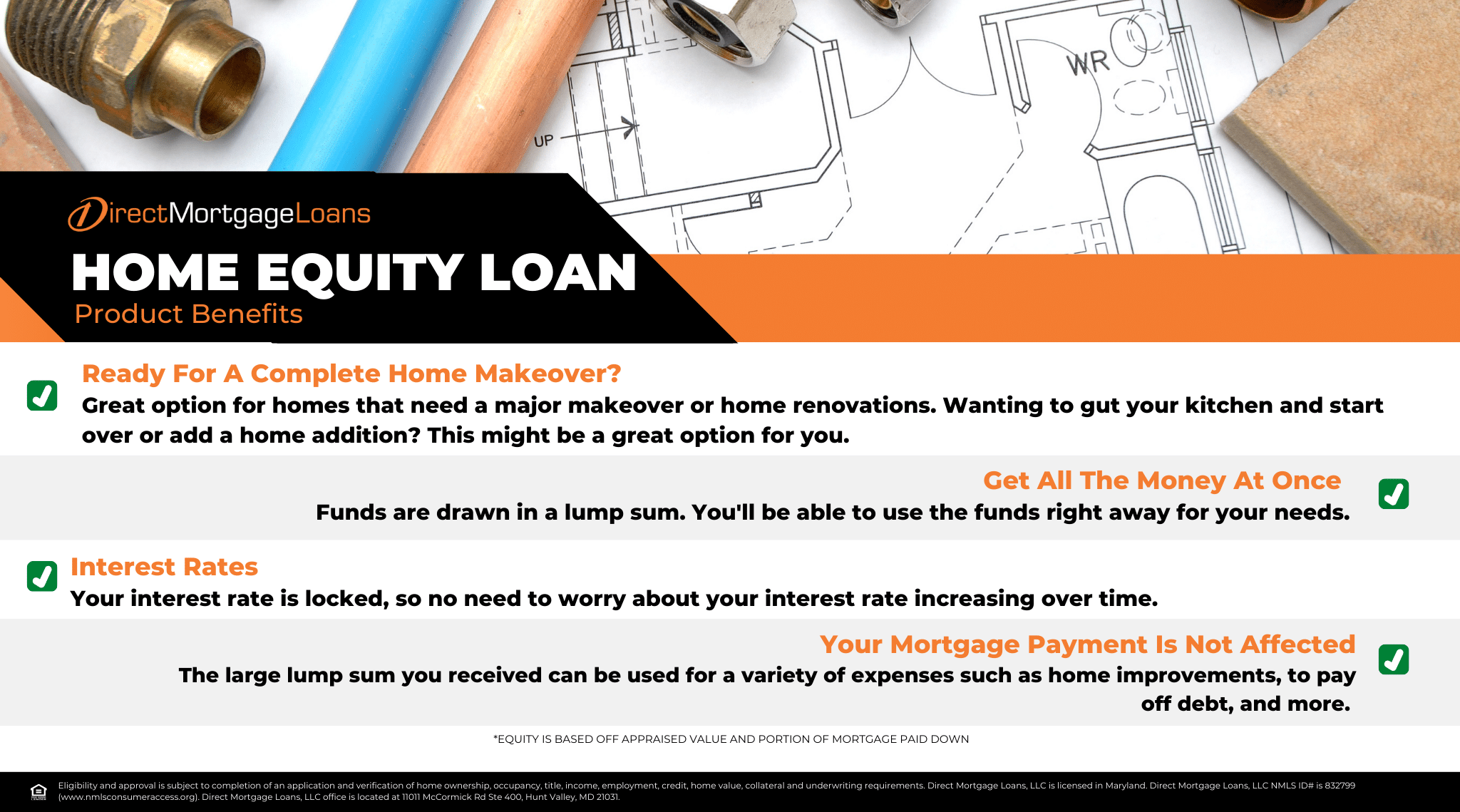

A home equity loan allows you to leverage your home’s built-up equity to finance various needs. The loan amount is based on your home’s value minus your remaining mortgage. You essentially borrow against this equity, using your home as collateral as security for the loan. You receive a lump sum in exchange and repay it in fixed monthly payments over a set term.

How does a home equity loan work?

A home equity loan functions like a second mortgage and is separate from your current loan. It allows you to borrow against your home’s equity and comes with its own set of loan terms, including a fixed interest rate and a separate monthly payment schedule.

Reasons To Get A Home Equity Loan

A home equity loan can be a useful tool for various needs, but it’s important to consider your financial situation and goals before applying. Here are some common reasons people use home equity loans:

- Home improvements: Home equity loans can be a good option if you want to make home improvements, such as adding a room or updating your kitchen. The improvements can increase the value of your home and provide a return on your investment.

- Consolidate Debt: If you have high-interest debt, such as credit card debt or personal loans, you can use a home equity loan to consolidate your debt into one payment with a lower interest rate.

- Unexpected expenses: If you have unexpected expenses, such as medical bills or home repairs, a home equity loan can provide the cash you need to cover the costs.

- Fund a large purchase: If you want to fund a large purchase, such as a car or a vacation, a home equity loan can provide the funds you need at a lower interest rate than other types of loans.

- Start a business: If you want to start a business, a home equity loan can provide the funds you need to get started.

Pros And Cons Of Home Equity Loans

If you’re thinking about using a home equity loan, it’s important to consider both the advantages and disadvantages before deciding. Here are a few factors to think about:

Advantages of a Home Equity Loan

Possible Lower Interest Rates: Typically, home equity loans offer lower interest rates compared to personal loans or credit cards because your home serves as collateral for the loan, making it less risky for the lender.

Predictable Fixed Payments: Home equity loans come with fixed interest rates. This predictability makes budgeting easier compared to loans with adjustable-rate mortgages (ARMs), as you’ll always know exactly how much your monthly payment will be.

Lump Sum Access for Large Expenses: Provide you with a one-time lump sum of cash. This is ideal for financing large expenses such as home renovations, college tuition, or consolidating high-interest debt into a single, lower-rate payment.

Potential Tax Benefits: In some cases, the interest you pay on a home equity loan may be tax-deductible if the funds are used for qualified home improvements. However, it’s important to consult with a tax advisor to see if this applies to your specific situation and tax filing status.

Disadvantages of a Home Equity Loan

Risk of Foreclosure: Since your home serves as collateral for the loan, missing payments can lead to foreclosure. This means you could lose your home if you face financial hardship and can’t make repayments.

Increased Debt: A home equity loan adds another debt obligation on top of your existing bills. Be sure you can comfortably afford the monthly payments alongside your current financial commitments.

Upfront Costs: Like your first mortgage, home equity loans often come with closing costs, including origination fees, appraisal fees, and title insurance. Factor in these upfront expenses when calculating the total loan cost.

Reduced Equity: As you borrow against your home’s equity, the portion of the home you truly own (your equity) shrinks. This can impact your ability to access other credit options in the future.

Home Equity Loan Options

Direct Mortgage Loans offers a variety of home equity loan options to help you unlock the potential of your home’s value. Here’s a breakdown of the key options to consider:

Piggyback (80-15-5)

This loan is taken alongside your main mortgage. It helps people with limited down payment savings to get extra funds so they can qualify for the primary mortgage without private mortgage insurance expenses.

Closed End

Closed-End Second Loans could be better for less risk-averse clients. They lack the flexibility of draws and initial lower initial payments like HELOCs but allow borrowers to tap into their home’s equity without having to worry about the interest rate changing with the market.

Stand Alone HELOC

Home Equity Lines of Credit (HELOC) give borrowers access to funds up to the equity value of their home.

How To Apply For A Home Equity Loan

Direct Mortgage Loans offers a variety of mortgage options, including home equity loans. Keep in mind that you will need to meet specific requirements based on the type of loan and the lender you choose. Here is a general overview of the steps to obtain a home equity loan.

- Application: Submit an application with details about your home’s value and your financial situation.

- Approval: The lender appraises your home to determine your equity, and approves the loan amount based on the appraised value and your specific financial situation.

- Closing & Access to Funds: Once approved, you’ll finalize the loan details. After closing, you can access the funds needed during the draw period.

- Repayment: After everything is finalized, you’ll begin making monthly payments that cover both the principal (original loan amount) and interest on the home equity loan.

FAQ’s on Home Equity Loans

Can you refinance a home equity loan?

You have the option to refinance your existing home equity loan with a new one if you qualify for a lower interest rate or better loan term. Alternatively, you can refinance your home equity loan into a home equity line of credit (HELOC) for more flexibility in accessing your funds.

It’s best to speak with a Loan Officer about your specific situation and explore the refinancing options available to you. They can help you determine if refinancing your home equity loan makes sense for your financial goals.

How much can I borrow on a home equity loan?

A home equity loan generally allows you to borrow around 80% to 85% of your home’s value, minus what you owe on your mortgage.

Is a home equity loan interest tax deductible?

In some cases, the interest you pay on a home equity loan may be tax-deductible if the funds are used for qualified home improvements. However, it’s important to consult with a tax advisor to see if this applies to your specific situation and tax filing status.

Is a home equity loan a good idea?

A home equity loan could be a good option if you need a moderate sum of funds and prefer a fixed repayment schedule with predictable monthly payments. Home equity loans often have slightly higher interest rates than refinanced mortgages, but they could be easier and faster to obtain since they don’t involve replacing your existing mortgage. They are also a good option if you don’t plan on staying in your home for a long time, as you wouldn’t need to recoup the refinancing costs associated with a cash out refinance.

How long does it take to get a home equity loan?

The time for a home equity loan application to be approved depends on the lender and your financial situation. It can take anywhere from a few days to a few weeks. Start your conversation with a Direct Mortgage Loans professional to discuss your home equity loan options.

Is a home equity loan a second mortgage?

Yes, a home equity loan is considered a second mortgage. Both types of loans use the equity in your property as collateral to secure the loan. The main difference lies in how you receive and repay the funds.