What is a credit check?

A credit check, also referred to as a credit pull, is a formal request to access your credit report. Lenders, creditors, and authorized entities are the typical initiators of these credit checks. There are two primary types: hard pulls and soft pulls. At Direct Mortgage Loans, we utilize both soft and hard credit checks to assess your loan eligibility. Now, let’s explore the distinctions between these credit checks and their impact on your credit score.

What is a soft credit pull?

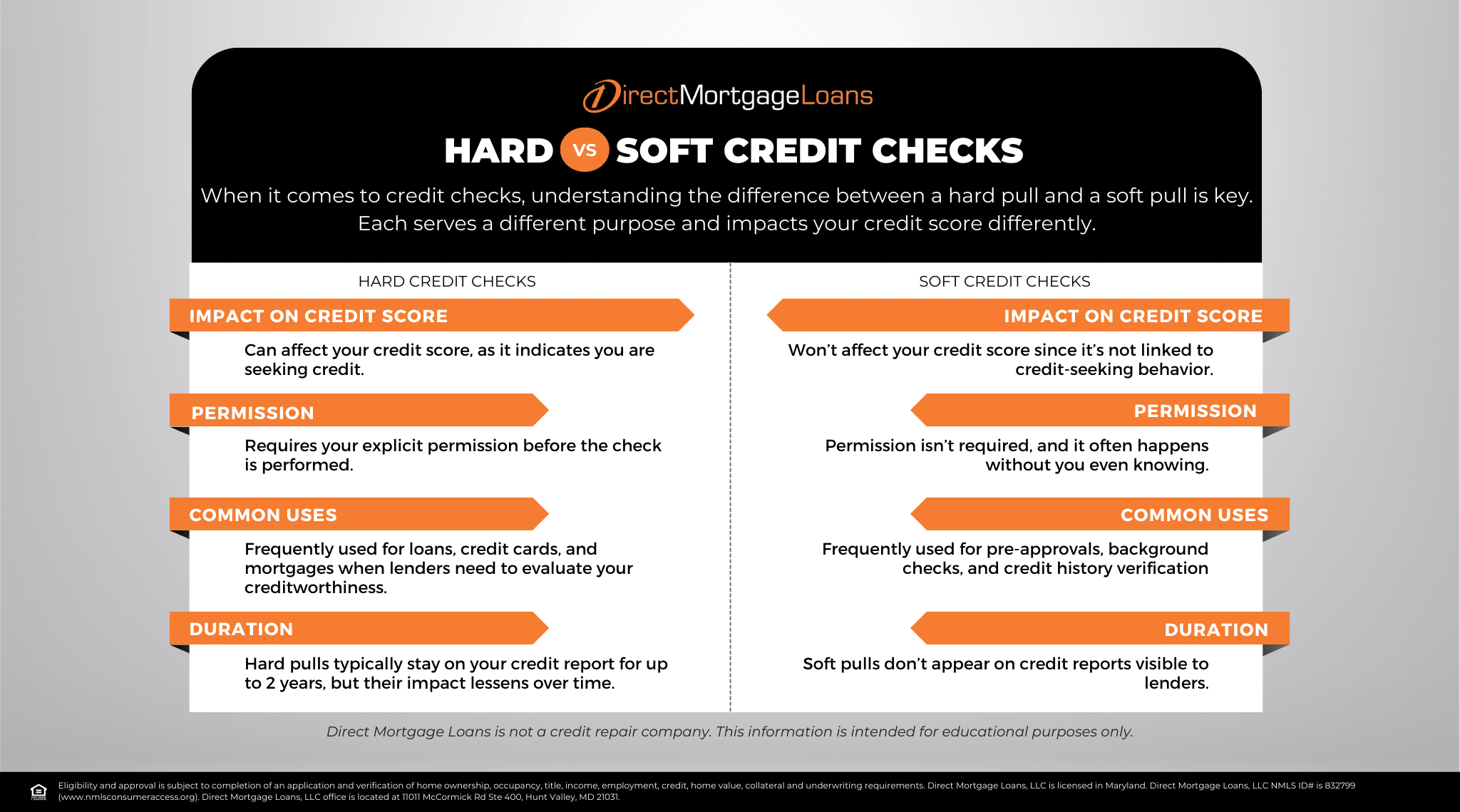

A soft credit pull, or soft inquiry, is a credit check that has no impact on your credit score. Lenders and financial institutions typically use soft credit pulls to pre-qualify you for loans or credit offers, and to evaluate your creditworthiness for purposes like employment or insurance. Moreover, soft credit pulls are only visible to you on your credit report.

What does a soft pull on credit show?

A soft pull on your credit shows basic personal information, a summary of your credit history, recent inquiries, any public records related to your credit, and sometimes a summary of your credit scores. It does not reveal detailed account-specific information and doesn’t affect your credit score. Specifically, soft inquiries are used for informational purposes, like background checks for employment or pre-qualified credit offers.

Do soft inquiries show up on credit reports?

Soft inquiries appear on credit reports but are typically only visible to the person whose report is being checked. They are not shared with other creditors or lenders reviewing the same report.

What is a hard credit pull?

Hard inquiries, often referred to as “hard pulls” or “hard credit checks,” typically happen when a financial institution, like a mortgage lender or credit card issuer, assesses your credit as part of a lending decision. These inquiries commonly occur when you apply for a mortgage, loan, or credit card, and you usually need to grant permission for them to be conducted.

What does a hard pull-on credit show?

A hard pull on your credit provides the entity conducting it with a comprehensive view of your credit profile. This includes your personal details, credit history, credit scores, recent inquiries, and any public records, such as bankruptcy.

How bad does a hard pull affect credit score?

A single hard inquiry may briefly lower your credit score, but it typically has a minor impact and won’t significantly affect your approval for a new credit card or loan. The negative effect on your credit score often subsides before the inquiry is removed from your credit reports (usually within about two years).

However, be cautious about applying for multiple credit cards at once or within a short timeframe, like a few months. Several inquiries in a brief period could make lenders and credit card issuers see you as a higher-risk borrower, possibly indicating financial strain or substantial debt. To maintain your creditworthiness, it’s a good idea to space out your credit card applications.

What does a hard pull show that a soft pull doesn’t?

A hard pull on your credit report provides more detailed information compared to a soft pull. It’s typically associated with applications for new credit like loans or credit cards, offering lenders a thorough view of your credit history and payment habits. This includes your credit scores, which soft inquiries usually don’t provide. Additionally, hard inquiries reveal your recent credit applications, giving mortgage lenders insights into your credit-seeking behavior.

Why do soft pulls and hard pulls exist?

Soft pulls are non-credit inquiries used for informational purposes, like self-checks or employment background checks. In contrast, hard pulls are credit inquiries during credit or loan applications, which can temporarily lower your credit score. Lenders use hard pulls to assess your creditworthiness. In mortgage lending, soft pulls could cut down on the amount of telemarketing calls from third parties when a hard credit pull occurs.

Soft Pulls vs Hard Pulls: FAQ’s

Are all credit inquiries reported on my credit report?

No, not all credit inquiries are reported on your credit report. Only hard inquiries, which occur when you apply for credit, are typically recorded. Soft inquiries, like checking your own credit or pre-approved credit offers, are not visible to lenders and do not appear on your credit report.

Can I remove hard inquiries from my credit report?

It’s challenging to remove legitimate hard inquiries from your credit report. They can stay on your report for a couple of years. However, if you believe a hard inquiry is inaccurate or unauthorized, you can dispute it with the credit reporting agencies.

Is it bad to have too many soft inquiries?

Having too many soft inquiries is generally not an issue, as they are typically for informational purposes and do not have an impact on your credit score. However, it’s important to be cautious about accumulating too many hard inquiries in a short period, as this can concern lenders.

Can lenders see soft pulls?

Lenders do not have access to soft pulls, and these inquiries do not appear in your credit report. Soft pulls are typically only visible to you.

How can I check my credit score?

- Choose a Reliable Source: Ensure you select a trustworthy source to check your credit score. The major credit bureaus – Experian, Equifax, and TransUnion – offer free annual credit reports at AnnualCreditReport.com. Additionally, some credit card companies, banks, and financial institutions provide free credit scores.

- Create an Account: If you’re using a website or app to access your credit score, you’ll typically need to set up an account. This process involves providing personal details like your name, address, and Social Security number.

- Request Your Score: After creating an account, request your credit score. The procedure may vary by the source but is usually straightforward.

- Review Your Score: Once you receive your credit score, carefully review it. Pay close attention to any negative information in your report, such as late payments or collections. If you spot any inaccuracies, promptly dispute them with the credit bureaus.

Additional Tips For Checking Your Credit Score

- Check your credit score regularly: It’s a good idea to check your credit score at least once a year, or more often if you’re planning to apply for a loan or other form of credit. This will help you track your progress and identify any potential problems early on.

- Be aware of different types of credit scores: There are many different types of credit scores, and lenders may use different types of scores when making lending decisions.

- Don’t be afraid to ask for help: If you have any questions about your credit score or how to improve it, don’t be afraid to ask for help from a financial advisor or credit counselor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.