When financing a home, it’s important to work with a company you know, like, and trust. While there are many mortgage companies, not all are the same; some are direct mortgage lenders and others are big banks. Both offer home loan services. At Direct Mortgage Loans, we are a direct mortgage lender that specializes in direct, personalized, and quick* loans to make homeownership available to you!

In this article, we will discuss the pros and cons of a direct mortgage lender and a big bank in terms of a mortgage loan.

Subscribe to our blog to receive notifications of posts that interest you!

What is a direct loan lender?

Direct lenders are “financial institutions that originate, process, and fund the loans themselves” (themortgagereports). There are many pros and cons to working with a direct loan lender.

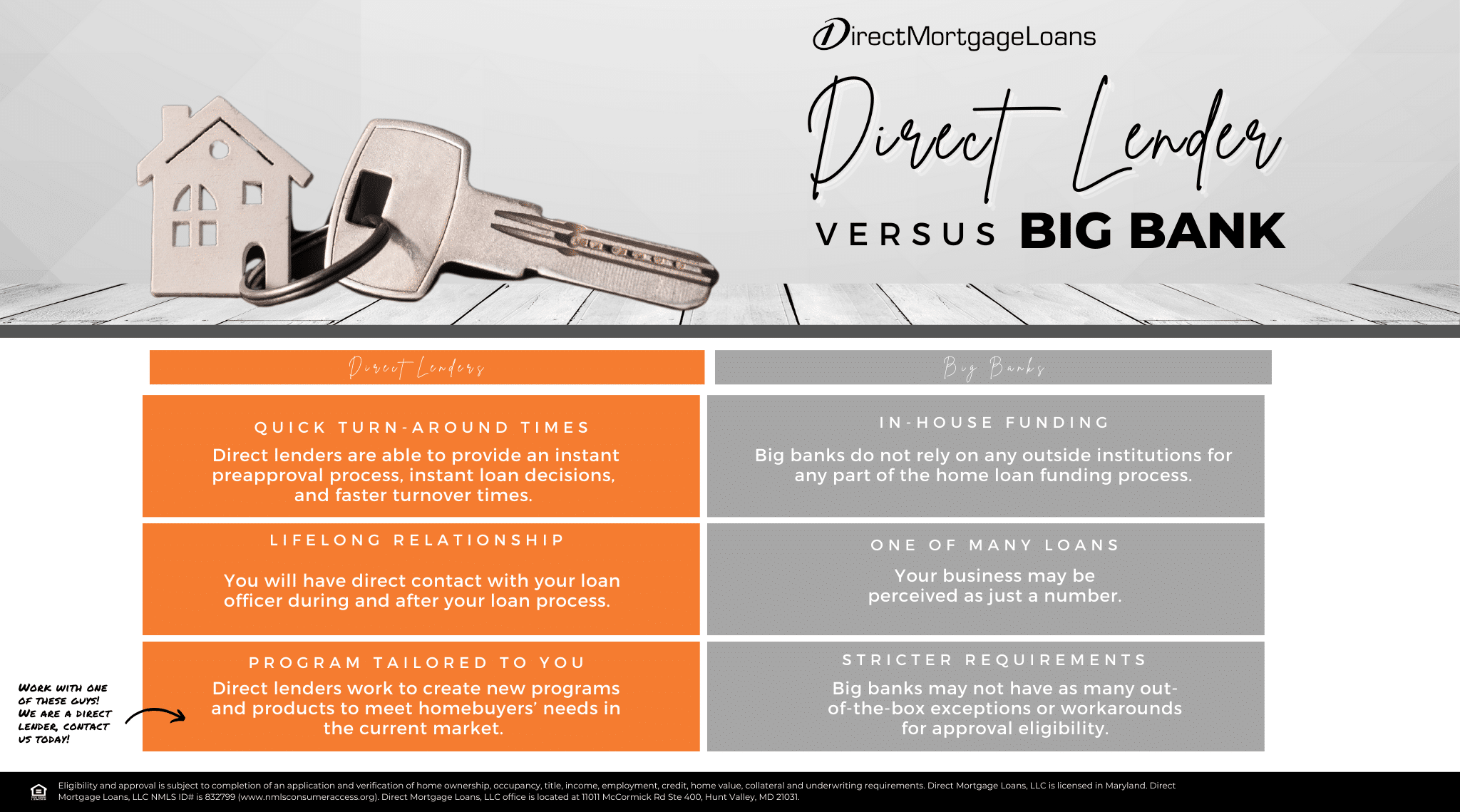

Direct loan lenders can make the whole home loan process very quick and efficient. Since direct lenders require fewer third parties and less paperwork, this calls for a more efficient process. Direct lenders may be able to provide an instant pre-approval process, instant loan decisions, and faster turnover times.

Direct lenders tend to lend to a wider range of borrowers. Where banks may turn applicants down based on stricter criteria, direct lenders may have access to additional programs with less strict guidelines.

Direct lenders create a more personable financial experience. At Direct Mortgage Loans, our loan officers work hard to continue a lifelong relationship with clients as their mortgage advisors! You will have direct contact with your mortgage lender during and after your loan process.

Many direct lenders work to create new programs and products to meet homebuyers’ needs in the current market.

The focus of a direct loan lender is the client and making homeownership possible for them through their mortgage services. The professional you work with will create a trustworthy relationship with you. In the stress of finding a home and moving, the last thing you want to do is stress about your mortgage interest rate and mortgage loan. With a loan officer you trust, you can relax knowing that they are working to find the best solution for you.

Direct Lender Loans

Pros Of Direct Lender Loans

- Specialist loan officers who understand mortgage rate intricacies.

- More flexible with credit scores and loan options.

- May offer more competitive interest rates.

- Prioritizes your business and offers personalized service.

Cons Of Direct Lender Loans

- Limited to the loan programs they offer.

- If the lender is smaller or less well-known, there may be less online resources or customer reviews to help guide your decision.

Big Banks

Large banks also lend money to borrowers to buy a home — a mortgage loan. “Big banks are large, multi-billion-dollar financial institutions that offer a wide range of financial products such as deposit accounts and credit cards, in addition to mortgages” (freeandclear).

Since banks are large institutions, they have the financial means to potentially offer lower interest rates. This is beneficial if you clearly meet and exceed the criteria for pre-approval. A lower interest rate means a lower monthly mortgage payment.

Since banks handle the whole process from start to finish. They do not rely on any outside institutions for any part of the home loan funding process. This can create an efficient process for having your loan closed.

However, while banks can potentially offer a lower rate, there are major downsides. One is that your business may be perceived as just a number. They are “big banks” for a reason and have millions of customers. Unlike a loan officer, big banks may not have the time or the bandwidth to provide customized mortgage solutions.

In addition, big banks may have stricter requirements and there may not be as many out-of-the-box exceptions or workarounds for approval eligibility. If you do not have the stated credit score, down payment, and income a big bank requires, you may be turned down.

Get a FREE quote with us today!

Bank or Credit Union Mortgage

Pros

- Wide range of services beyond mortgage loans, like credit cards and savings accounts.

- Generally have more established reputations and a larger online presence.

Cons

- May have stricter requirements for credit scores.

- Tend to have less competitive mortgage rates.

- Service can be less personalized due to their institutionalized nature.

Direct Loan Lender vs. Bank: Key Differences

When it comes to securing a mortgage loan for real estate, you might find yourself stuck at a crossroads: choosing between a direct loan lender like Direct Mortgage Loans, and a bank or credit union. This decision often comes down to personal preferences and circumstances, but understanding the difference between a mortgage company and a bank can greatly simplify the choice.

A direct mortgage lender, as the name suggests, works directly with you to fund your loan. In contrast, big banks and credit unions tend to act as a middleman between the borrower and the loan originator. The main goal of a direct mortgage lender is to make the process as straightforward as possible for the borrower. While a bank may have more institutional constraints due to their size and nature.

One key aspect to consider in the mortgage lender vs bank debate is the way interest rates are handled. Direct lenders can sometimes offer more competitive mortgage rates because they are more flexible and focused on mortgage loans, whereas banks have a broader spectrum of services, like credit cards and savings accounts, to manage.

Moreover, if your credit score isn’t particularly strong, a direct lender might be more willing to work with you and provide you with loan options suitable for your financial situation. Big banks, on the other hand, may have stricter criteria and be less flexible when it comes to credit scores.

Mortgage lenders play a crucial role, too. In direct lending companies, the loan officers are often specialists in mortgage lending and can guide you through various loan programs. Meanwhile, in banks, you might interact with generalists who handle different types of loans.

In conclusion, the choice between lenders vs banks for your mortgage loan depends on your personal mortgage goals and current financial portfolio. Whether you opt for a bank loan or a loan from a direct loan lender like Direct Mortgage Loans, make sure the choice is right for you.

Speak With A Direct Mortgage Lender Near Me!

Rates are subject to change. Eligibility and approval are subject to completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral, and underwriting requirements. Direct Mortgage Loans, LLC NMLS ID# is 832799 (www.nmlsconsumeraccess.org). Direct Mortgage Loans, LLC office is located at 11011 McCormick Rd Suite 400 Hunt Valley, MD 21031. Equal housing lender.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.