Are you in the market for a new home? It’s important to know your financing options. While conventional loans are a popular choice for many, if you’re considering a more expensive property, a jumbo loan could be a better option. This article will break down the main differences between jumbo vs conventional loan types. It will also walk you through how they function, outline their specific requirements and help you figure out which one might be the best fit for you.

Subscribe to our blog to receive notifications of posts that interest you!

What is a jumbo mortgage loan?

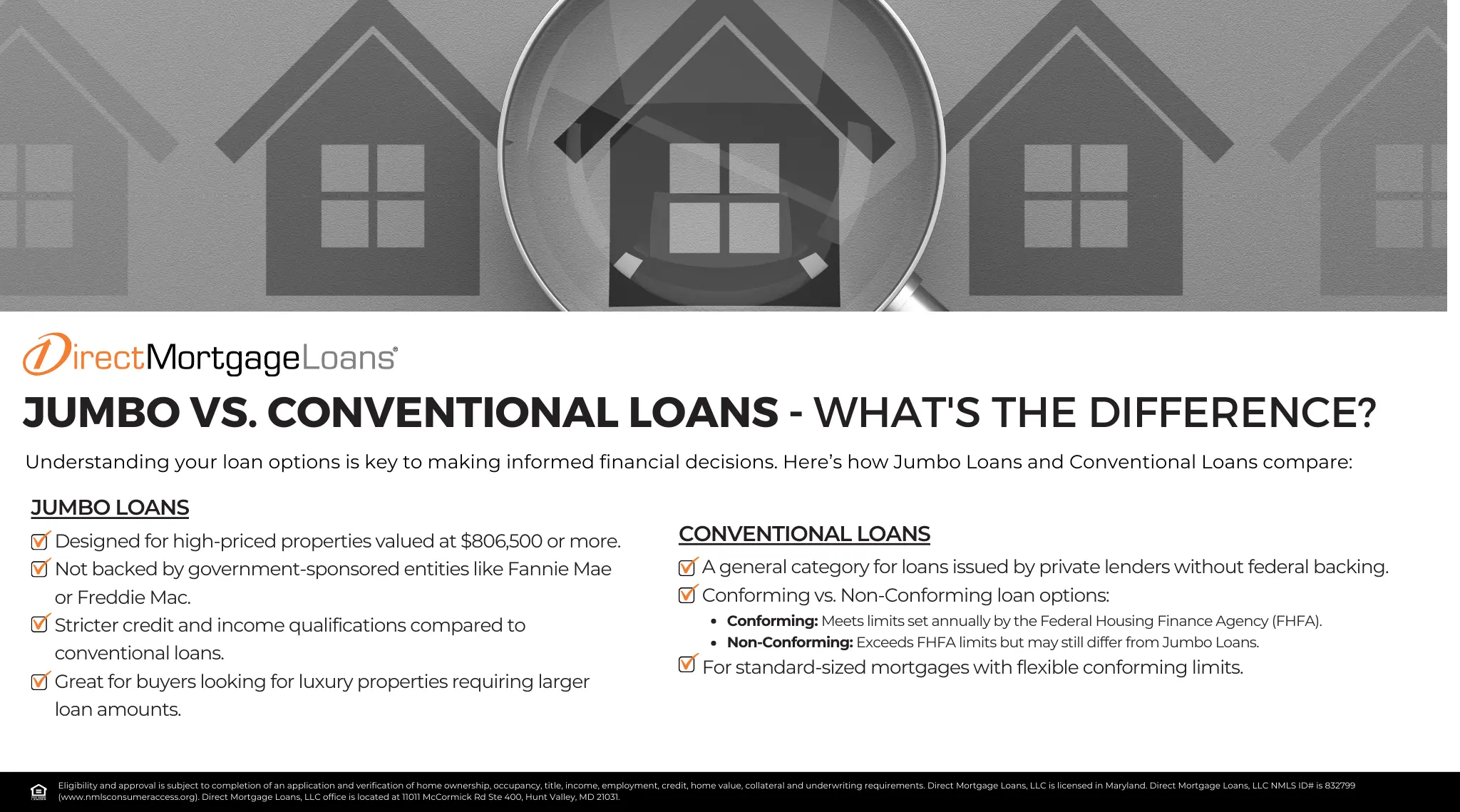

Jumbo loans are designed for borrowers buying a home that exceeds the conforming loan limit set annually by the Federal Housing Finance Agency (FHFA). These loans, also known as non-conforming, do not adhere to the lending guidelines established by Fannie Mae and Freddie Mac. Jumbo loans provide flexibility and can be used for various properties, including primary residences, vacation homes, investment opportunities, and second homes.

What is a conventional mortgage loan?

Conventional loans are a popular option for homebuyers due to their flexibility and ability to accommodate a variety of financial situations. Unlike government-backed loans, conventional loans lack government insurance. However, they typically adhere to standards established by Fannie Mae and Freddie Mac, conforming to the loan limits set by the Federal Housing Finance Administration (FHFA).

Difference: Jumbo vs Conventional Loan:

The main difference between jumbo and conventional loans is their borrowing limits. Conventional loans follow guidelines set by the Federal Housing Finance Agency (FHFA). In 2024, the limit is $766,550 in most areas, but the limit could go up to $1,149,825 in higher-cost areas. In simpler terms, if the home you’re buying is less than the FHFA limit, you’d probably choose a conventional loan over a jumbo loan.

Moreover, Government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac purchase conventional loans, giving lenders more flexibility with qualification requirements. As a result, conventional loans often offer lower interest rates compared to jumbo loans.

On the contrary, jumbo loans exceed the conforming limits set by the FHFA and do not have any backing from GSEs. This increases the risk for lenders, leading to stricter financial requirements. These requirements may include a higher credit score, a larger down payment, and a lower debt-to-income ratio (DTI).

Fixed-Rate Mortgage

Fixed-rate mortgages have the same interest rate for the entire duration of the loan. This means that the monthly mortgage payment, covering the loan principal and interest, remains consistent. Typically, fixed loans come with terms of 15 or 30 years and are a popular option for someone who plans on staying in their home long term.

Adjustable-Rate Mortgage

An adjustable rate mortgage (ARM), also known as a variable-rate mortgage, is a type of home loan where the interest rate can change over time. Unlike a fixed rate mortgage, which keeps the same interest rate throughout the loan period. Adjustable interest rate could fluctuate up or down based on market conditions. This means your monthly mortgage payments may increase or decrease, depending on how the interest rate changes.

What are the advantages of a jumbo loan?

Jumbo loans come with several advantages for borrowers seeking larger loan amounts. Let’s explore some of the key benefits:

Jumbo Loans Pros

- Financing higher loan amounts: Designed to finance properties exceeding the conforming loan limits, which allows one to borrow larger amounts to purchase higher-priced homes or investment properties.

- Flexibility in property types: Can be used to finance a variety of property types, including single-family homes, luxury residences, vacation homes, and investment properties.

- Customized loan terms: These loans could offer more flexibility in terms of repayment options. Borrowers can choose from various loan terms such as fixed-rate or adjustable-rate mortgages and customize the repayment schedule to fit their financial goals and needs.

- Expanded home buying opportunities: By accessing larger loan amounts, jumbo loans enable you to consider properties in high-cost markets or desirable neighborhoods where home prices exceed the conforming loan limits.

What are the disadvantages of a jumbo loan?

While jumbo loans offer various benefits, they also come with a few potential drawbacks borrowers should consider.

Jumbo Loan Cons

- Stricter qualification requirements: Obtaining a jumbo loan is more challenging due to stricter qualification requirements and a lengthier, potentially more extensive underwriting process than securing a conforming loan.

- Higher down payment: Typically requires a larger down payment, usually at least 20% of the home’s purchase price, which may pose affordability challenges.

- Potential for higher interest rates: Due to higher risk, jumbo loans may carry slightly higher mortgage interest rates, although competitive rates are attainable for borrowers with strong credit profiles.

- Market volatility impact: Jumbo loans are more susceptible to market volatility. In the event of a market downturn, properties financed with jumbo loans can lose value, which may result in negative equity and financial instability for borrowers.

Jumbo Loan Requirements

The requirement for a jumbo loan may vary depending on the mortgage lender. However, here are a few of the basic requirements.

- Credit Score: Lenders usually look for a credit score of 700 or higher, indicating responsible borrowing history.

- Debt-to-Income Ratio (DTI): It’s recommended for your DTI to be under 45% to ensure you can easily manage your loan payments along with your other financial responsibilities.

- Cash Reserves: The specific amount needed will be based on your credit score, loan-to-value ratio (LTV), and DTI, but you should aim to have at least 6 months’ worth of mortgage payments readily available.

- Down Payment: Jumbo loans typically require a minimum down payment of 20%.

What are the advantages of a conventional loan?

Conventional loans offer several advantages for borrowers seeking mortgage financing. Let’s explore some of the key benefits:

Conventional Loan Pros

- Range of down payment options: Offers down payment flexibility, with options ranging from 3%- 20%, making homeownership more accessible.

- Mortgage Insurance Flexibility: Mortgage insurance is not required for purchases with 20% down or more. This could save you a significant amount over the life of the loan. If you put down less than 20%, you can work with your loan officer to determine the mortgage insurance option to best fit your scenario.

- Less stringent requirements: Compared to other loan types, conventional loans have relatively lenient criteria, favoring borrowers with good credit scores, stable employment, and reasonable debt-to-income ratios.

What are the disadvantages of a conventional loan?

While conventional loans offer several advantages, they also come with a few potential drawbacks borrowers should consider.

Conventional Loan Cons

- Stricter Credit Requirements: These types of loans tend to have stricter credit score requirements while also requiring a lower debt-to-income ratio, making qualifying more difficult for some borrowers.

- Potential for Higher Interest Rates: Lower credit scores or higher risk could result in higher interest rates and increased monthly payments.

- Limited Government-Backed Guarantees: Unlike FHA, USDA, and VA loans, conventional loans lack government-backed guarantees, potentially affecting borrower support during financial hardships or defaults.

Conventional Loan Requirements

To be eligible for a conventional loan, you must meet specific requirements. Here is a general overview.

- Credit Score: A minimum credit score of 620 is necessary to qualify for a loan, but this requirement could differ depending on the lender.

- Debt-to-Income Ratio (DTI): Most lenders prefer the DTI for conventional loans to be below 50%.

- Down Payment: For conventional loans, down payments can range from 3% to 20%. However, the specific amount depends on your financial situation, loan type, and the property you’re planning to purchase.

- Private Mortgage Insurance (PMI): If you make a down payment of less than 20%, you will need to pay PMI until you reach the required property value.

Are jumbo mortgage rates higher than conventional?

Typically, jumbo loan rates are higher than conventional loan rates. Since jumbo loans carry higher loan amounts and pose higher risks to lenders, they often come with higher interest rates. Additionally, jumbo loans may require larger down payments and stricter qualification criteria compared to conventional loans. It’s important to consult with your loan officer for a clear understanding of the specific terms and conditions for jumbo loans in your area.

What type of buyer should consider a jumbo loan?

Jumbo loans could be ideal for borrowers who need more flexibility in financing and have the financial means to meet stricter requirements. Here are a few types of buyers who might consider a jumbo loan:

- High-income earners: Jumbo loans allow you to borrow more to purchase your dream home, even if it exceeds conforming loan limits.

- Homeowners who want to upgrade: If you want a bigger home that doesn’t meet loan limits, or if you’re buying a property in an area with very high home prices.

- Investors and developers: Jumbo loans can be used to finance investment properties or high-value development projects.

What type of buyer should consider a conventional loan?

Conventional loans are a popular choice for many buyers because they offer different down payment options. Nevertheless, these loans are best for buyers with higher credit scores, a manageable debt-to-income ratio, and a stable income and work history. Here are a few other types of buyers who should consider a conventional loan.

- First-time homebuyers: Conventional loans offer down payments as low as 3%, making them an attractive option for first-time home buyers looking to enter the market.

- Buyers with a 20% down payment: By putting down 20% or more, you’ll avoid private mortgage insurance (PMI), which can save you money in the long run.

- Buyers financing a moderately priced home: If your desired home falls within the conforming loan limit for your area, a conventional loan offers could offer favorable loan terms.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.