If you’re planning to buy a home, closing costs are one of the most important line items to understand before you get to the finish line. These fees are charged at the closing of a real estate transaction, and they can add thousands of dollars to your total upfront costs.

The good news: knowing what to expect puts you in control. This guide breaks down everything you need to know about closing costs on a mortgage, including what’s included, who pays them and how to cover them without breaking the bank.

Subscribe to our blog to receive notifications of posts that interest you!

What are closing costs on a house?

Mortgage closing costs are the fees that are charged when you buy or sell a property. These fees may include all third-party fees incurred during the mortgage process (title search fees, home appraisal fees, lender fees, attorney fees, etc.) which will be itemized on your loan estimate and closing disclosure. Closing costs can also include taxes and insurance premiums. The amount of your closing costs will depend on a number of factors, such as the price of the property, the type of loan you have, and the location of the property. In general, closing costs can range from 2% to 5% of the purchase price of the property.

If you are still early in the process, our Mortgage FAQs and Home Buyer Guide are good places to start.

What Is a Closing Disclosure?

A Closing Disclosure is the document that outlines the final terms and costs of your mortgage. It details every fee, shows who pays and receives money at the closing table and must be made available to you at least three business days before settlement.

Review it carefully. Compare it line by line against your Loan Estimate. You can use our Mortgage Calculators to sanity-check the numbers before closing day.

Why Closing Costs Matter

Closing costs can add up to thousands of dollars, and they are often an afterthought for buyers focused on the down payment. Understanding them upfront helps you budget accurately and gives you room to negotiate. Missing them can mean scrambling for cash at the worst possible moment.

If you have not yet started the approval process, knowing your closing cost range early can shape how you approach getting pre-approved and what documents you will need to gather.

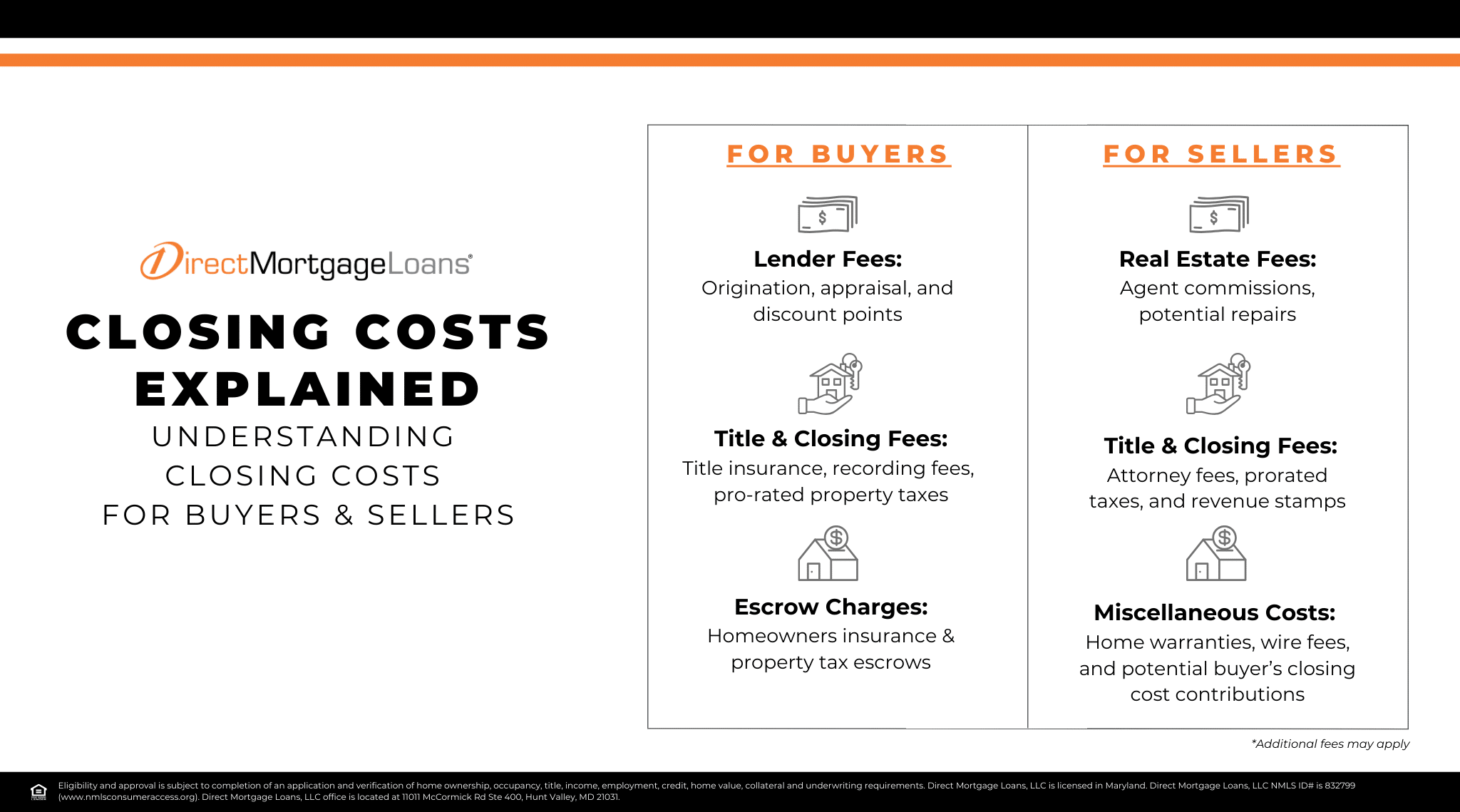

What Is Included in Closing Costs?

Here is a breakdown of the most common fees you can expect:

Appraisal Fee

Covers the cost of a licensed appraiser evaluating the property’s fair market value. This is typically paid by the buyer. Understanding what hurts home appraisals can help you avoid surprises that affect your final loan terms.

Escrow Fee

An escrow account is managed by a third party to hold funds until all conditions of the transaction are met. It also ensures your property taxes and homeowners insurance are paid on time throughout the year.

Home Inspection Fee

Covers the cost of a professional inspector evaluating the property for structural issues, safety concerns or damage. Knowing what to look for during a home inspection can help you use this step strategically, not just as a checkbox.

Property Taxes

Prepaid property taxes begin at the date of closing and run through the end of the tax period.

Loan Origination Fee

This fee covers the cost of processing and underwriting your loan. It typically runs around 1% of the total loan amount and appears in the origination charges section of your Loan Estimate.

Underwriting Fee

Covers the lender’s cost to evaluate your creditworthiness and assess the risk of the loan.

Credit Report Fee

The cost of pulling your credit report as part of the loan review process. If you are unsure where your credit stands, read up on what credit score is needed to buy a house before you apply.

Title Search Fee

Covers the cost of verifying the property’s ownership history to confirm the title is clear of any liens or claims.

Private Mortgage Insurance

Depending on your loan type and down payment, you may owe PMI. It helps to understand the difference between private mortgage insurance and lender-paid mortgage insurance so you know what you are paying for and why.

Homeowners Insurance

Many lenders require the first year’s premium to be paid at or before closing.

Attorney Fees

If an attorney represents you during closing, their fees are included in your closing costs. (Required in some states.)

Recording Fees

The cost of recording the sale and mortgage documents with the local government.

Transfer Taxes

Some states charge a transfer tax when property changes hands. This varies by location.

How to Pay for Closing Costs

There are several ways to cover closing costs. Here are the most common options:

Pay From Your Checking or Savings Account

If you have the funds available, this is the most straightforward approach. Those funds need to have been in your account for at least 60 days before closing.

Roll Them Into Your Mortgage

Depending on the loan, you may be able to add closing costs to the loan balance. This reduces what you need at closing, but you will pay interest on that amount over the life of the loan. It can also affect your loan-to-value ratio, so talk to your loan officer before deciding.

Ask for Seller Credits

In a buyer’s market, sellers may agree to cover some or all of your closing costs. Read more about what seller concessions are and how to ask for them without weakening your offer.

Use Gift Funds

Family members can contribute to your closing costs through a gift fund. If you plan to use gift funds, coordinate with your loan officer early. Read our full guide on gift funds for down payment to understand the process.

Apply for Down Payment Assistance

Many state and local programs can help cover both your down payment and closing costs. DML offers access to down payment assistance programs across multiple states. Learn more about what down payment programs are available to you.

Buy Down Your Rate

Some buyers use funds at closing to purchase discount points and lower their interest rate. Our guide to buying down your mortgage rate explains how it works and when it makes sense.

What to Do Right After Closing

Once you have closed on your home, a few important steps will help you get settled quickly:

- Get copies of all closing documents, including the Closing Disclosure and loan paperwork.

- Change the locks on all exterior doors.

- Update your driver’s license address within 30 days (check your state’s MVA requirements).

- Set up utilities in your name with a transfer date matching your closing date.

- Forward your mail at usps.com.

- Update your address with employers, banks, credit card companies and other businesses.

- File for any applicable property tax exemptions within 30 days of closing. Our guide to mortgage interest deductions can help you maximize your tax benefits in the first year.

Frequently Asked Questions About Closing Costs On A House

Can you negotiate closing costs?

Yes. You can negotiate with the seller to cover some or all of your closing costs. Reviewing five things to know when submitting an offer can help you approach that conversation strategically.

How much should you budget for closing costs?

Plan for 2% to 5% of the purchase price. Your loan officer can give you a more precise estimate. Use our Mortgage Calculators to model different scenarios.

When do you pay closing costs?

Closing costs are paid at settlement, the final step in the transaction where the title transfers from seller to buyer.

Can you roll closing costs into your mortgage?

In some cases, yes. This reduces your upfront cash requirement but increases the total amount you finance and the interest you pay over time. Talk to a loan officer to understand whether this option makes sense given your loan type and financial goals.

What happens if my mortgage application is denied?

If something unexpected comes up during underwriting, here is what you can do if your mortgage application is denied and how to move forward.

*Eligibility and approval is subject to completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral and underwriting requirements. Direct Mortgage Loans, LLC NMLS ID# is 832799 (www.nmlsconsumeraccess.org). Direct Mortgage Loans, LLC office is located at 11011 McCormick Rd Suite 400 Hunt Valley, MD 21031. Equal housing lender.*

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.