A major benefit of VA loans is that they’re assumable, offering advantages for both buyers and sellers. In this blog, we’ll cover how a VA loan assumption works, what you need to know, and the pros and cons to help you make an informed decision.

Subscribe to our blog to receive notifications of posts that interest you!

Can a VA loan be assumed?

Yes, VA loans are assumable. This means a qualified buyer could take over an existing VA mortgage from a home seller. The buyer inherits the original loan terms, including the interest rate and monthly payment.

What is a VA loan assumption?

A VA loan assumption is a method to buy a home by taking over someone else’s existing VA mortgage. Instead of going through the traditional mortgage process, the buyer simply takes over the terms of the original loan. This means, the buyer keeps the same interest rate and monthly payment as the previous homeowner. The new borrower takes on the responsibility for the remaining loan balance and agrees to make all future payments.

Who can assume a VA loan?

Anyone who meets the lender’s financial qualifications can assume a VA loan. This means you don’t have to be a veteran or currently serving in the military to take over an existing VA mortgage. Lenders typically have requirements such as minimum credit score and income levels that must be met.

VA Loan Assumption Requirements

To assume a VA loan, the borrower taking over the loan must meet certain qualifications. Keep in mind, specific requirements could vary depending on the mortgage lender.

- Credit Score: The buyer will need to meet the lender’s minimum credit score requirement.

- Income: The buyer must demonstrate sufficient income to comfortably afford the monthly mortgage payments.

- Funding Fee: Typically, a 0.5% funding fee is required, unless the buyer qualifies for an exemption due to a service-related disability.

- Loan Assumption Liabilities: The buyer agrees to take on all financial responsibilities associated with the loan.

How to assume a VA loan?

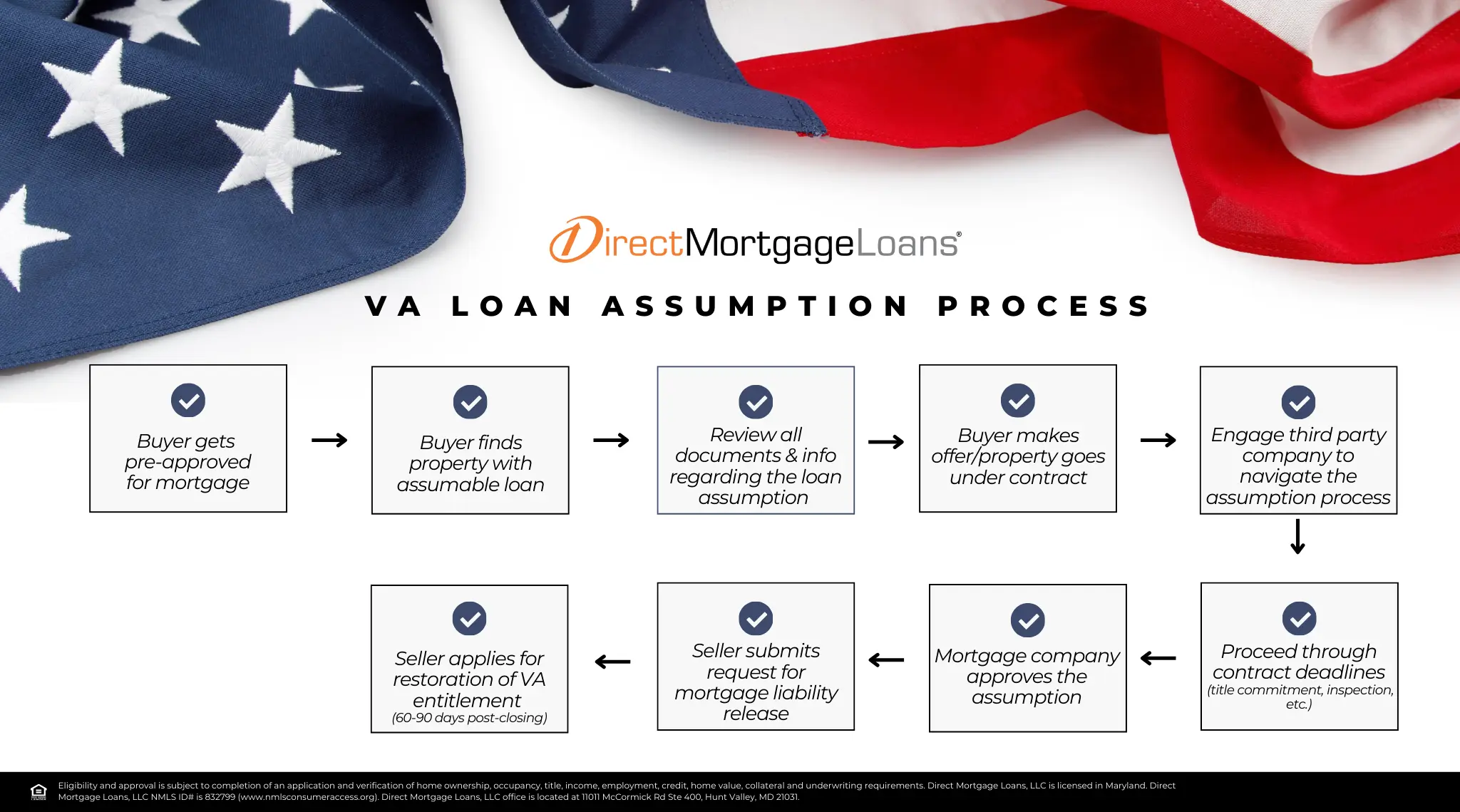

If you are interested in assuming a VA loan, then there are some general steps you can follow.

- Find an Assumable Loan: Work with your real estate agent to find a property with an assumable loan.

- Gather Information: Get details on the seller’s current mortgage balance and interest rate. This helps you determine affordability and the potential savings from assuming the loan.

- Make an Offer: Include a contingency in your offer specifying your purchase is conditional on assuming the existing VA loan.

- Submit Paperwork: Provide the lender with documents like proof of income, debt information, and bank statements, just as you would for a new loan.

- Wait for Approval: The lender will review your qualifications and the assumption request before finalizing the process.

How To Find VA Assumable Loans

To find VA assumable loans, there are a few options available. One option is to work with a real estate agent who has MLS access, making it easier to find homes with assumable mortgages. Alternatively, search major real estate websites where sellers may highlight assumable loans in their listings.

VA Loan Entitlement After An Assumption

Your VA entitlement determines the maximum loan amount you can qualify for without a down payment. When you sell a home with a VA loan, the process of transferring the loan to a new owner is called an assumption. The new buyer’s VA entitlement status will determine how your entitlement is affected:

- Substitution of Entitlement: If the new buyer is a veteran with VA entitlement, then they may be able to substitute their entitlement for yours. This means your entitlement is freed up for use on another property.

- No Substitution: If the new buyer doesn’t have VA entitlement, then your entitlement will remain tied to the home until the loan is paid off or refinanced. This could limit your ability to use your VA benefit for another home purchase.

Release Of Liability After A VA Loan Assumption

When transferring your VA home loan to someone else, the buyer must agree to take on all your loan responsibilities. To be released from this obligation, the seller can include a loan assumption statement in the deed of transfer or have the buyer sign a separate legal agreement. Both options must be approved by the VA. It’s best to consult with your Loan Officer and lawyer to ensure a smooth process to secure your release of liability from the VA.

VA Loan Assumption Pros and Cons

Just like any mortgage option, it’s important to weigh the pros and cons to determine if a VA loan assumption is right for you.

Pros Of Assuming A VA Mortgage

Assuming a VA loan could provide several benefits for both sellers and buyers. Here are some of the key advantages:

- Cost Savings: Buyers could save by avoiding closing costs, appraisal fees, and mortgage insurance.

- Attractive Interest Rates: If the original loan has a lower rate than current market rates, then assuming it can lead to significant long-term savings.

- Restoration of VA Benefits: When a VA loan is assumed by a veteran, the seller can reclaim their full VA loan benefits, allowing them to use these benefits again in the future.

- Accessibility for non veterans: VA loans can be assumed by non veterans, increasing the pool of potential buyers for the home.

Cons Of Assuming A VA Mortgage

While there are several benefits, there are also some drawbacks to consider. Here are some to be aware of:

- Impact on Seller’s VA Entitlement: If a non veteran buyer assumes the loan, then the seller’s VA entitlement remains tied to the original loan until it’s fully repaid.

- Lender Approval Required: Not all lenders approve VA loan assumptions automatically. Each request must be reviewed, which could extend the home selling process.

- Liability Risks: If the buyer defaults on the loan, then the original borrower might still be held liable unless the lender formally releases them from the obligation.

VA Assumable Loan FAQ’s

How long does it take to assume a VA loan?

The time it could take to assume a VA loan will depend on the lender and the buyer’s specific situation. The process could take anywhere from 60 days to 4 months or up to a year, depending on the complexity of the loan.

Can a non veteran assume a VA loan?

Yes, a non veteran could assume a VA loan if they meet the lender’s financial requirements. This allows someone who doesn’t normally qualify for a VA loan to take over an existing VA mortgage. However, there are risks for the veteran homeowner in doing this. If your VA entitlement is still tied to the original loan, then you won’t be able to use your benefits again until the loan is fully repaid.

Are all VA loans assumable?

Typically, VA loans originated on or after March 1, 1988, can be assumed by a qualified buyer. However, both the lender (and potentially the VA) must approve the assumption.

Do you have to be a vet to assume a VA loan

No, you do not have to be a veteran to assume a VA loan. As mentioned earlier, anyone can assume a VA loan regardless of their military service history. However, the lender will need to approve the assumption based on the borrower’s credit score and other financial factors.

How many times can you assume a VA loan?

You could assume a VA loan as many times as you have available entitlement. This means that if you meet the VA’s eligibility requirements and have remaining entitlement, then you could assume a VA loan multiple times.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.