Is it cheaper or more expensive to build or buy a house?

As of June 2023, the median sales price for new houses sold was $415,400, with an average sales price of $494,700. When building a house, the cost depends on factors like size and location. On average, constructing a new home cost around $150 per square foot. Here’s an approximate cost breakdown for different house sizes:

Discover your financing options with DML’s construction loans!

Cost Considerations: Building a House vs Buying

Before deciding whether to buy an existing home or build a new one, consider the cost factors for each option:

Cost of Building a New House

- Land Plot: Factor in the expense of acquiring the land for construction.

- Home Financing: Secure funding for the construction project.

- House Plans & Design Fees: Include expenses for developing house plans and architectural services.

- Permits & Inspection Fees: Account for costs associated with obtaining necessary permits and complying with local regulations.

- Labor: Allocate the price for hiring skilled professionals, including the general contractor and laborers.

- Site Work/Excavation: Budget for costs of preparing the construction site.

- Foundation & Framing: Consider expenses for building a stable foundation and structural framework.

- Utilities & Finishes: Include costs for essential utilities and finishing the house’s interior and exterior.

- General Maintenance & Unexpected Costs: Plan for miscellaneous expenses and general maintenance throughout the construction process.

Cost of Buying a House

- Home Inspection: A thorough inspection could identify potential issues before finalizing the purchase of the home.

- Maintenance & Repairs: Budget for higher maintenance and repair costs, especially for aging elements like roofs and gutters.

- Less-Efficient Major Appliances: Older homes may have less energy-efficient appliances, leading to higher utility bills.

- HOA Fees: If part of a homeowner’s association, there will be HOA fees for communal amenities and services.

Start your application to begin your homebuying journey!

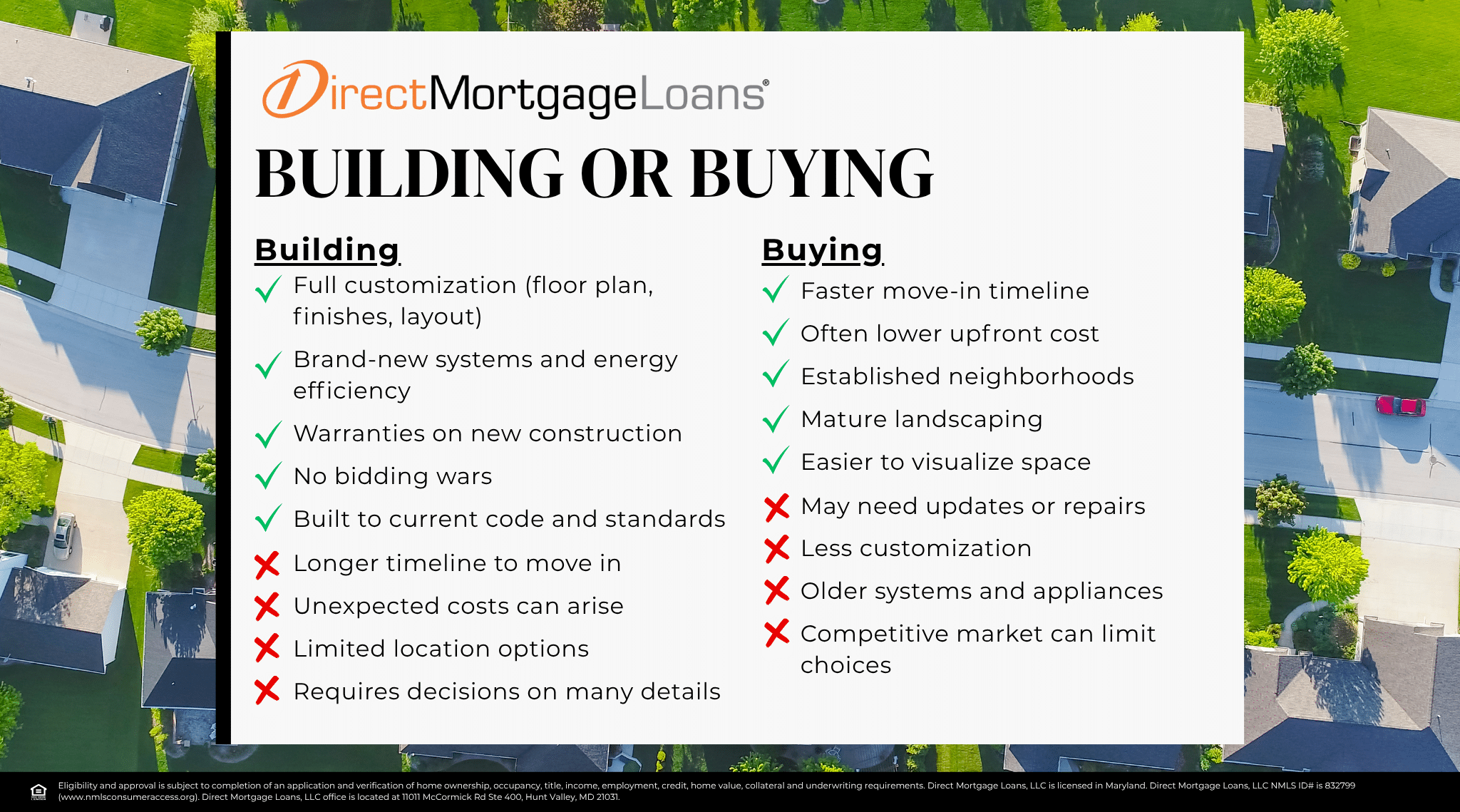

Building A New Home: Pros and Cons

Having examined the expenses associated with purchasing and constructing a new home, it is time to delve into the advantages and disadvantages of each option.

Pros of Building a New House

- Personalization: You have full control over the design to match your preferences.

- Reduced Competition: Avoid bidding wars commonly experienced in the existing home market.

- Lower Maintenance: Newer homes can come with warranties for major systems and appliances.

- Modern, Safe Materials: No worries about hazardous substances found in older homes.

- Better Energy Efficiency: Building an energy-efficient home can cut down on your home’s energy usage and electricity bills.

Cons of Building a New House

- Can Be Stressful: The process of building a new home requires hands-on involvement and can be demanding and stressful at times.

- Unexpected Costs and Delays: Unforeseen expenses and construction delays are common in new home construction.

- Lengthy Build Time: Building a new home takes much longer than buying an existing home.

- Limited Negotiating Power: Unlike the resale market, new homes can offer limited flexibility with closing costs or purchase price.

Apply for a Construction Loan today!

Buying An Existing Home: Pros and Cons

If you’re considering buying an existing home, here are the advantages and disadvantages to review.

Pros of Buying an Existing Home

- Faster Move-In: Often quicker closing process allows you to move in sooner.

- Room to Negotiate: You can negotiate the price and discuss repairs with the seller.

- Less Risk: The overall process is usually easier, and home loans are less risky than land loans.

- Renovating over Time: Flexibility to renovate and improve the property gradually.

Cons of Buying an Existing Home

- Unforeseen Issues & Repairs: Aging homes may have hidden repair expenses.

- Compromise on Wants & Needs: Finding a perfect match may require compromising on certain features.

- Environmental Concerns: Older homes may have environmental issues, such as harmful substances like lead paint or asbestos.

- More Competition: In a competitive real estate market, desirable existing homes may face more competition, leading to bidding wars and higher prices.

How to Decide If Building or Buying a Home Is Right for You

When deciding between an existing home and a newly constructed one, consider the actual monthly cost of owning your home beyond the sales price. Newly built homes often result in lower energy bills and require less maintenance, potentially reducing your monthly expenses. Additionally, paying more in interest each month may offer an added tax benefit.

Use the calculator to compare the true costs of owning an existing home versus a newly constructed one.

Building A House vs Buying A House FAQ’s

How do I finance the construction of a new build home?

Direct Mortgage Loans offers One-Time Close Construction-To-Permanent Loans to finance the construction of your newly built home. This program combines interim construction financing, lot purchase, and permanent loan into one, making it accessible with lower credit and down payment options.

With the permanent loan closing before construction begins, there’s no need for borrower requalification or additional costs like a second appraisal or closing. It simplifies the process of building your dream home and offers convenience and peace of mind!

What are the requirements for obtaining a construction loan?

FHA Requirements

- Maximum LTV: 96.5%

- 15 and 30-year fully amortized fixed.

- 620 minimum qualifying credit score.

- New multi-wide manufactured modular housing, 1-unit stick-built housing.

USDA Requirements

- Maximum LTV: 100% of market value

- 30-year fully amortized fixed.

- 620 minimum qualifying credit score.

- New multi-wide manufactured modular housing, 1-unit stick-built housing.

VA Requirements

- Maximum LTV: 100% not including VA funding fee

- 15 and 30-year fully amortized fixed.

- 620 minimum qualifying credit score.

- New multi-wide manufactured modular housing, 1-unit stick-built housing.

Are there any government programs or incentives for financing new build homes?

Yes, several government programs and incentives are available to encourage homeownership and stimulate the construction industry. Learn more about the Down Payment Assistance Programs you may qualify for!

Scenarios where a construction loan may be the right option for you:

- Building a Custom Home: If you have plans for a custom home, a new construction loan can provide the necessary financing for your construction costs.

- Building a Spec Home: As a developer or builder constructing a spec home (a home built before selling), a new construction loan can cover the expenses of construction.

- Locking in Your Interest Rate: With a new construction loan, you have the advantage of locking in your interest rate before construction begins, ensuring certainty for future mortgage payments.

- More Control in Construction: Gain greater control over the construction process, collaborating with the builder to meet your specific preferences and standards.

- Large Down Payment: New construction loans typically require a larger down payment than traditional mortgages. If you have substantial savings for a down payment, this option may suit you well.

Regardless of whether you decide to build a new house or buy an existing one, you can trust us to handle your home financing needs. Get in touch with one of our expert Loan Officers to explore your options today!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.