Are you considering a FHA loan for your home purchase? These loans are a popular option among homebuyers due to their lower down payments and flexible credit requirements. In this guide, we’ll break down the pros and cons of FHA loans to help you decide if it’s the right fit for your homeownership journey.

Subscribe to our blog to receive notifications of posts that interest you!

What is FHA mortgage?

A FHA mortgage is a type of loan insured by the Federal Housing Administration (FHA), which allows lenders to be more flexible with their requirements for borrowers who may not meet traditional criteria. These loans are commonly used by first-time homebuyers and can have either a fixed or adjustable interest rate.

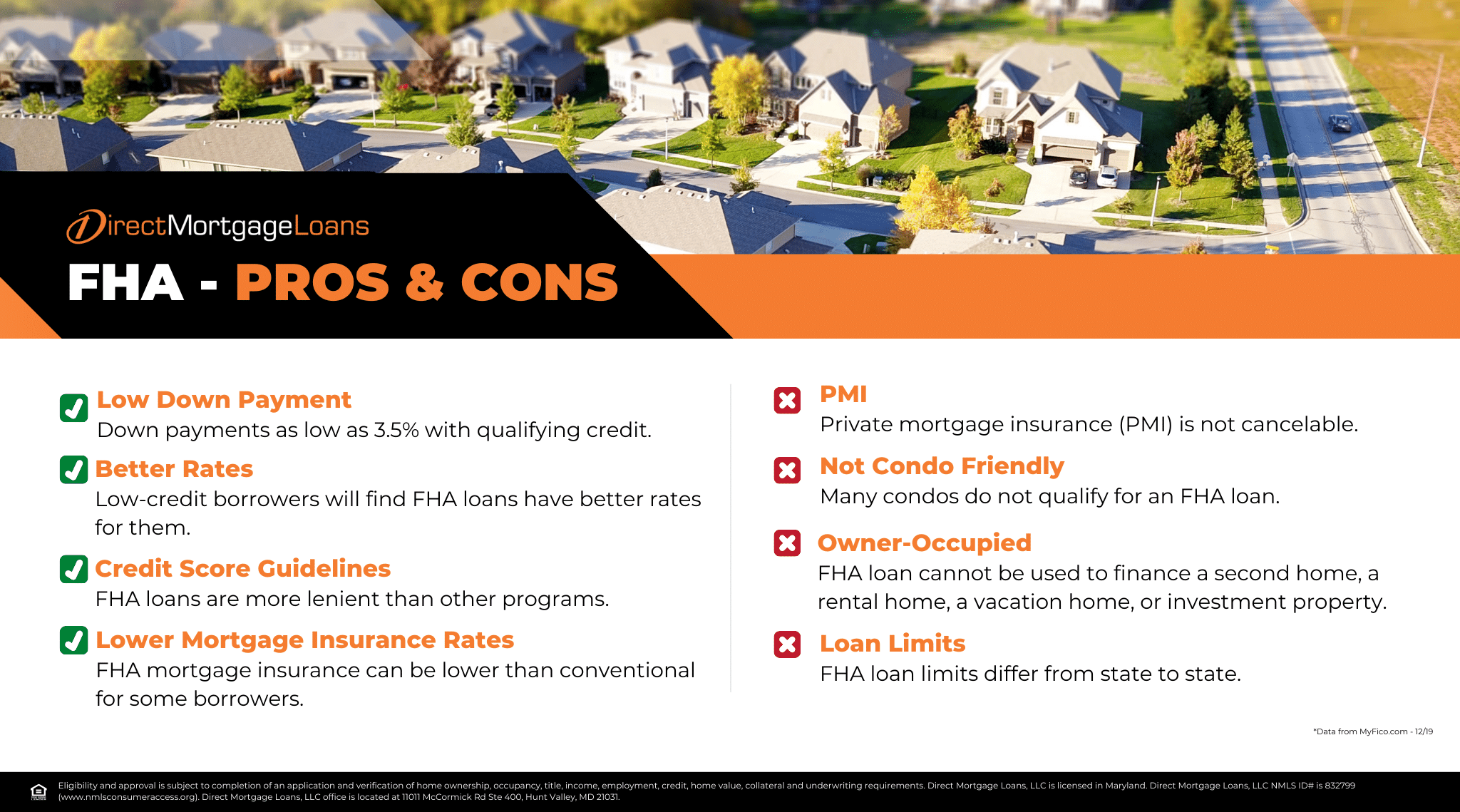

Pros and Cons of FHA Loan

If you’re thinking about using an FHA loan, it’s important to consider the pros and cons to help you determine if this option is right for you.

Advantages of FHA Loan

There are several advantages that make FHA Loans a popular option among home buyers. Let’s take a closer look at benefits:

Lower Down Payment

One of the main advantages of FHA loans is the lower down payment requirement. With a credit score of 580 or higher, you could qualify for a down payment as low as 3.5%. Even with a credit score between 500 and 579, you might only need a 10% down payment.

To further assist with upfront costs, FHA loans allow the use of gift funds from family or friends towards the down payment. Additionally, you may be eligible for down payment assistance programs offered by government agencies or local organizations.

Competitive Interest Rate

FHA loans often come with more competitive interest rates compared to conventional loans. This is because the Federal Housing Administration (FHA) insures the loan, reducing the lender’s risk. As a result, lenders can offer more favorable terms to borrowers. You also have the flexibility to choose between a fixed-rate or an adjustable-rate mortgage (ARM).

Credit Score

FHA loans are known for being more forgiving when it comes to credit scores. You could qualify for a down payment as low as 3.5% with a FICO score of 580 or higher. Even with a credit score as low as 500, you may qualify with a 10% down payment.

Higher DTI

FHA loans tend to be more forgiving of higher debt-to-income ratios compared to conventional loans. While the preferred DTI is 43%, you might qualify with a DTI up to 57% depending on other factors. This flexibility can be especially beneficial for borrowers with large amounts of debt.

Support for Home Improvement Projects

The FHA 203(k) loan offers support for homebuyers purchasing properties that require renovations. This program combines financing for the home purchase and necessary improvements into a single mortgage. By streamlining the process, you could avoid needing a separate loan to cover renovation costs.

Disadvantages of FHA Loan

While FHA loans offer several benefits for first-time homebuyers and those with less-than-perfect credit, it’s essential to consider the potential disadvantages as well.

FHA Loan Limits

One limitation of FHA loans is the maximum loan amount you could borrow. These limits are established by the Federal Housing Administration and vary depending on the location. In most areas of the country, the maximum loan amount is $472,030. However, in high-cost housing markets, the limit can be significantly higher, reaching up to $1,089,300. There are also special exceptions for Alaska, Hawaii, Guam, and the U.S. Virgin Islands, where the FHA loan limit for single-family homes is capped at $1,633,950.

Property Requirements and Restrictions

To qualify for this type of loan, the property must meet specific property standards set by the FHA to ensure safety, security, and structural soundness. Before finalizing the purchase, an FHA appraisal is required to verify the property’s compliance with these guidelines and determine its value. If the property fails the inspection, the deal could fall through.

Mortgage Insurance Premiums (MIP)

FHA mortgage insurance protects lenders in case of borrower default. It consists of two components: an upfront premium paid at closing and an annual premium included in your monthly mortgage payment. The upfront premium is typically 1.75% of the loan amount. The annual premium varies based on factors such as loan term, amount, and loan-to-value ratio (LTV).

How can I get pre approved for an FHA loan?

To get pre approved for an FHA loan, there are some general steps you can take:

- Contact an FHA-Approved Lender: Start by reaching out to a lender approved by the Federal Housing Administration (FHA). They will evaluate your financial situation to determine if you qualify for an FHA loan.

- Gather Necessary Documentation: Collect all required documents, such as proof of income, tax returns, bank statements, and identification, to complete your mortgage application.

- Submit Your Application: Provide the gathered documentation to your lender and submit your mortgage application.

- Receive Pre Approval Letter: After reviewing your application, your lender will issue a pre approval letter stating the loan amount you qualify for.

FHA Loan FAQ’s

Is it worth it to get an FHA loan?

A FHA Loan could be a good option for first-time home buyers of those with limited funds for a down payment and a lower credit score. Nevertheless, there are also some drawbacks to consider as well like private mortgage insurance. It’s best to consider your specific situation and contact a Loan Officer to determine if this loan option is a good choice for you.

Can I refinance my FHA loan?

Yes, you could refinance your FHA loan with either an FHA streamline refinance or a cash-out refinance. The FHA streamline refinance lets you refinance your existing FHA-insured mortgage without requiring an appraisal. On the other hand, a cash-out refinance allows you to access your home equity as cash. To determine the best option for you, it’s best to speak with a Loan Officer.

What documentation is required for an FHA loan application?

To apply for a FHA loan, you will need to provide a range of financial documents. These documents help the lenders evaluate your financial situation and decide if you qualify for a mortgage. Typically, you will need to submit tax returns, W-2 forms, recent pay stubs, bank statements, and asset statements. Additionally, you will be required to authorize a credit check.

What types of FHA loans are available?

There are various types of FHA loans available, each with their own set of requirements and benefits. Here’s a general overview of the most common FHA loan options:

- Home Purchase: FHA loans are commonly used to finance the purchase of single-family houses, townhouses, or condominiums. This option is ideal for first-time homebuyers due to its lower down payment requirements and credit score criteria.

- FHA Rate Term Refinance: You could refinance your current FHA loan to get a lower interest rate or change the loan term. This could help you save money each month and pay off your mortgage sooner.

- FHA Streamline: This option allows refinancing without an appraisal, providing a fast and simple process for borrowers with existing FHA-insured mortgages.

- FHA Cash Out Refinance: With an FHA Cash Out Refinance, you could convert your home equity into cash. This extra money can be used for debt consolidation, home improvements, or other financial needs.

- FHA 203(k): Ideal for those buying a fixer-upper, FHA 203k loans combine the cost of the home and renovations into one mortgage. This simplifies the financing process by avoiding the need for a separate renovation loan.

- FHA 100% Financing: This program offers 100% financing for FHA loans, so no down payment is needed (though closing costs still apply). It combines a first and second mortgage, with the second mortgage covering up to 3.5% of the sales price or appraised value, whichever is lower, and having a term of 10 years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.