Buying a second home can be an exciting journey, but it’s important to approach the decision with careful planning. This article explores key factors to consider and offers guidance on how to navigate the process of purchasing a second home.

What is a second home?

A second home is a property you own in addition to your primary residence, and it is intended for you to live in throughout the year. You can use it for vacations, weekend getaways, or even work retreats. Unlike an investment property that generates income through rentals, a second home is meant for personal use. However, occasional rentals are allowed with some restrictions.

To qualify as a second home, the IRS typically requires you to spend at least 14 days or 10% of the rental days (whichever is greater) at the property each year. Additionally, it’s usually at least 50 miles away from your primary residence.

Subscribe to our blog to receive notifications of posts that interest you!

What can you use second homes for?

There are various uses for a second home, such as vacation homes, secondary residences, and investment properties. Let’s explore each of these in more detail.

Vacation Home

Vacation homes are a popular choice for individuals looking to purchase a second home. Whether it’s a cabin in the woods or a beachfront condo, a vacation home could provide the perfect getaway space.

Secondary Residence for Work

If you frequently travel for work, you might want to consider buying a second home in the city where you often spend time. Accommodation costs such as hotels can add up quickly, so having a secondary residence for work purposes could be a beneficial option to explore.

Investment Property

Owning a second home could be a good investment. Renting out your property when you’re not using it could help pay for ownership costs or even make a profit. You can consider long-term leases or short-term vacation rentals. Remember that investment properties may have different mortgage requirements and tax implications compared to vacation homes or secondary residences.

Is buying a second home a good investment?

When considering whether buying a second home is a good investment, it’s important to take several factors into account. Location plays a crucial role, so researching market trends and future appreciation projections is essential.

It’s also important to consider potential hidden costs such as ongoing maintenance, property taxes, and periods of vacancy. Consulting with an expert real estate agent and Loan Officer is recommended as they can offer valuable insights into specific market dynamics, financing options, and potential returns on investment.

Pros And Cons of A Second Home

If you’re considering a second home purchase, weigh the advantages and disadvantages. Here’s a breakdown of some pros and cons of a second home to help you make an informed decision:

Pros of Purchasing a Second Home

- Home Away from Home: A second home offers the comfort and convenience of having your own space for getaways at your leisure. It’s a place where you can relax and recharge, without the hassle of negotiating someone else’s terms.

- Potential Rental Income: If your second home sits in a desirable location with high tourist traffic, you could leverage short-term rental platforms like Airbnb to generate income when you’re not using the property. This could help offset ownership costs and potentially even turn a profit.

- Investment Potential: Real estate, like most investments, has the potential for appreciation. Over time, the value of your second home may increase, offering a return on your investment.

Cons of Purchasing a Second Home

- Financial Strain: Owning a second home is a significant financial commitment. In addition to the initial purchase price, there are ongoing costs such as the down payment, mortgage payments, closing costs, property taxes, and insurance that you will be responsible for paying.

- Stricter Requirements: Qualifying for a second home loan could be more difficult than a primary residence. These loans tend to have higher mortgage interest rates and a larger down payment requirement.

- Selling Challenges: Selling a second home could be a slower process compared to primary residences. Market fluctuations and location could make selling your second home more difficult.

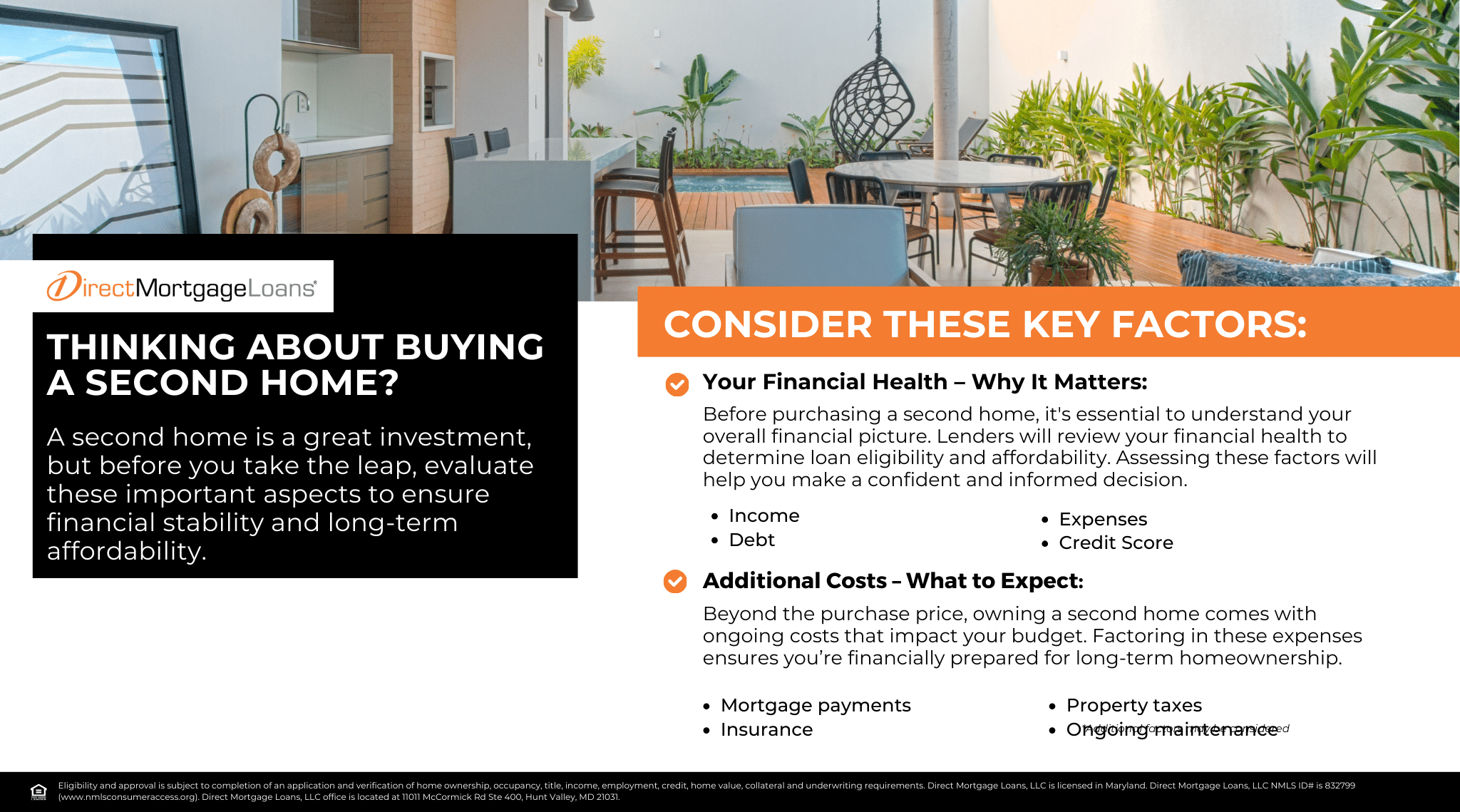

Can I afford to buy a second home?

To determine if you can afford a second home, it’s best to speak with a Loan Officer to discuss your personal financial situation. However, there are several financial factors to consider that can help you determine if purchasing a second home is a wise decision.

When purchasing a second home, you will likely need to make a larger down payment and could expect higher mortgage interest rates compared to your primary residence. This is due to the slightly higher risk for lenders.

Additionally, it’s important to keep your debt-to-income ratio below 43% to qualify for a second mortgage. Consider additional expenses such as property taxes, homeowner’s association fees (if applicable), and maintenance. Ensure that you can manage the monthly payments along with your current expenses

How To Buy A Second Home

If you’re looking to purchase a second home, there is a lot to consider. Here is a general overview of the steps you need to take when purchasing a second home.

- Determine Your Goals: Be clear about your property goals. Determine if it will be a weekend retreat, a family gathering spot, or an investment property. This will heavily influence your location choice, property type, and financing.

- Financing Options: Common mortgage options for second homes include conventional and jumbo loans. It’s best to speak with a Loan Officer to figure out the best option for your financial situation. Keep in mind that compared to government-backed loans for primary residences, these options usually have stricter lending requirements.

- Get Pre-Approved: Gather your documents and apply for pre-approval. This will give you a clear picture of your affordability range and show the seller that you’re a qualified buyer.

- Find a Home: Work with a knowledgeable real estate agent to find a second home that meets your needs. They will assist you in locating a property and guide you through the negotiation and offer process.

- Make an Offer: Once you find the perfect second home, work with your agent to make a competitive offer. They can help with negotiation strategies and make sure all the terms are clear

- Close on Your Second Home: After your offer is accepted, a closing day will be scheduled, which involves signing paperwork and finalizing the mortgage.

Second Home Mortgage Requirements

The mortgage requirements for a second home vary based on the chosen loan type and mortgage lender. However, there are general requirements to keep in mind.

- Down Payment: Be prepared to put down at least 10% of the purchase price. This is higher than the minimum required for primary residences because lenders consider second homes a bit riskier.

- Credit Score: Lenders may also have stricter credit score requirements for second homes. Generally, you’ll need a score of at least 620, but a higher score could lead to better loan terms.

- Debt-to-Income Ratio (DTI): This ratio shows how much of your income goes towards monthly debt payments. A lower DTI (ideally below 43%) indicates a stronger financial position and could improve your chances of qualifying for a loan.

Is buying a second home right for you?

Purchasing a second home can offer a range of personal and financial benefits. For some, it’s a place to escape on weekends or holidays. For others, it may serve as a future residence or a way to explore rental opportunities.

However, owning an additional property also comes with added responsibilities. These may include ongoing costs like mortgage payments, property taxes, insurance, maintenance, and association fees, depending on the location.

Before making a decision, it’s important to carefully consider your financial situation, long-term goals, and how a second home fits into your overall plans. With thoughtful planning, a second home can be a meaningful addition to your lifestyle and future.

FAQ’s About Purchasing A Second Home

Is it harder to buy a second home?

Second homes are usually more difficult to qualify for compared to primary residences. This is because the lender is taking on additional risk by providing a second loan on the property. If you are unable to pay off your mortgage and your property is foreclosed, the second mortgage is at a greater risk of not being fully paid.

Can I buy a second home with a VA loan?

VA loans can only be used to finance your primary residence. Although you typically cannot buy a second home with a VA loan, there are exceptions. For example, military members on the move might use a VA loan for their new home before selling their old one.

Moreover, if you’ve completely paid off your first VA loan, you might be able to use your remaining entitlement for a second home that you’ll live in full-time. Regardless of the situation, it’s important to talk to a VA loan specialist to see if you qualify for an exception.

What is the difference between investment property and second home?

If you’re thinking about buying a property that’s not your primary residence, it’s important to understand the differences between the different types of homes available, specifically investment homes and second homes.

The main difference between a second home and an investment home is how you plan to use it. A second home is for your personal enjoyment, like for vacations, weekends, or seasonal getaways. Whereas an investment home is purchased with the goal of generating income by renting it out to tenants, and it is not intended for personal occupancy.

Furthermore, second home mortgages usually have better loan terms, like lower interest rates, compared to mortgages for investment properties. Lenders typically view second homes as less risky because you have a personal stake in maintaining the property.

Can I buy another house while owning a house?

It is possible to purchase another house while still owning one. The key is to ensure you qualify for financing and can comfortably manage the additional costs of another property. This involves meeting the lender’s requirements for a new mortgage and carefully considering your financial situation to determine if carrying two mortgages or managing the ongoing expenses of another property aligns with your budget.

Does a mortgage on a second home cost more?

When you receive a mortgage for a second home, the out-of-pocket expenses will usually cost more than a mortgage for your first home. This is because the interest rates and down payment requirements for second mortgages are generally higher than those for first mortgages.

Lenders typically see second mortgages as riskier because they are providing an additional loan on the same property. If you cannot pay off your mortgages and your property is foreclosed, the second mortgage is at a greater risk of not being fully paid.

Can you deduct second home mortgage interest?

The interest on the mortgage for your second home may be tax-deductible if you use the property for personal use. However, there are limits on the deductible amount of mortgage debt based on IRS guidelines. It’s best to consult with a tax advisor to determine if your second home mortgage qualifies for a tax deduction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.