Are you a homeowner looking to access funds for renovations, debt consolidation, or other expenses? A home equity line of credit (HELOC) might be a good option for you. Let’s explore what a HELOC is, how it works, and how to qualify.

Subscribe to our blog to receive notifications of posts that interest you!

What is a HELOC Loan?

A Home Equity Line of Credit (HELOC) is a loan that lets you borrow money using the equity in your home as collateral. Your home’s equity is the difference between its market value and the amount you still owe on your mortgage. Like a credit card, a HELOC gives you a credit limit that you can use over a set period, usually 10 years, called the draw period. During this time, you only pay interest on the amount you borrow.

While HELOCs are like credit cards, there’s an important difference between the two; these types of loans are secured by your home, so if you can’t repay the loan, the lender could take possession of your property.

Is a HELOC loan a second mortgage?

A home equity line of credit (HELOC) is a type of second mortgage. This means it’s a loan you take out using your home’s value as collateral to access funds. However, unlike a traditional second mortgage that provides a lump sum, a HELOC offers a credit limit that you can use as needed during a draw period.

How does a HELOC loan work?

A Home Equity Line of Credit (HELOC) works like a revolving credit line that is secured by the equity in your home. Essentially, you are borrowing against the value of your home, minus the amount you still owe on your mortgage. Mortgage lenders typically allow you to borrow up to 85% of this equity.

These types of loans can be broken down into two key phases:

HELOC Loan Draw Period

This initial period, usually lasting 10 years, allows you to access funds from your home equity credit line as needed. You only pay interest on the amount you borrow during this time. This provides flexibility for ongoing projects or unexpected expenses.

HELOC Loan Repayment Period

After the draw period ends, you enter the repayment period, typically lasting 20 years. During this phase, your monthly payments will cover both the principal amount you borrowed and the accrued interest.

It’s important to remember that a HELOC is a loan secured by your home. If you fail to repay, the lender could foreclose. Therefore, responsible use and ensuring you can afford the repayments are crucial before tapping into your home’s equity.

Are HELOC loan rates fixed?

HELOCs typically have a variable interest rate, also known as an adjustable interest rate. Meaning the interest rate on the second loan can change over time. It’s important to keep this in mind when budgeting for your monthly mortgage payments, as payments may increase in the future.

HELOC Loan Requirements

Qualifying for a HELOC involves meeting some basic eligibility requirements, which could vary depending on your lender. Typically, you must have at least 20% equity in your home. Additionally, lenders will also review your credit score and history to see if you manage debt well. Your debt-to-income ratio is also an eligibility factor considered to ensure you can comfortably afford the HELOC repayments.

How To Get a HELOC Loan

Direct Mortgage Loans provides various mortgage options, including a home equity line of credit (HELOC). Although the steps may vary by lender, here is an overview of the process.

- Application: Submit an application with details about your home’s value and your financial situation.

- Approval: The lender appraises your home to determine your equity, and approves the loan amount based on the appraised value and your specific financial situation.

- Closing & Access to Funds: Once approved, you’ll finalize the loan details. After closing, you can access the funds needed during the draw period.

- Repayment: After everything is finalized, you’ll begin making monthly payments that cover both the principal (original loan amount) and interest on the HELOC.

How much HELOC loan can I get?

The amount you can borrow with a Home Equity Line of Credit (HELOC) depends on your specific situation. Typically, you can borrow up to 85% of your home’s value, minus the amount you still owe on your mortgage. To better visualize this, let’s consider an example:

Imagine your home is worth $500,000 and you still owe $300,000 on your mortgage. Meaning you’ve built up $200,000 in equity ($500,000 value – $300,000 owed).

Lenders typically allow you to borrow up to 85% of your home’s equity with a HELOC. In this case, 85% of $200,000 is $170,000. So with this scenario, the maximum HELOC you could qualify for would be $170,000.

However, other factors such as your credit score and debt-to-income ratio will also be considered to determine how much you are able to borrow with HELOC.

How To Calculate A HELOC Loan Payment

You can use our mortgage calculator, which allows you to compare the potential payments associated with a HELOC and a cash out refinance. Keep in mind that a HELOC typically includes a draw period of up to 10 years, during which you may be expected to pay only interest, followed by a repayment period. The calculator compares the costs during this repayment term.

How does paying back HELOC work?

Repaying a HELOC involves two stages. The draw period allows you to borrow from your approved credit line as needed and only requires you to pay the interest on the borrowed amount.

Once the draw period ends, the repayment period begins, which can last up to 20 years. During this time, your monthly payments will cover both the principal amount borrowed and the accrued interest. This usually results in higher payments compared to the draw period.

How long does it take to get a HELOC loan?

The process of obtaining a HELOC is similar to the refinancing process. On average, it takes around 30 days to complete. However, the timeframe can vary, with some cases being processed more quickly and others taking longer.

Is it a good idea to get a HELOC loan?

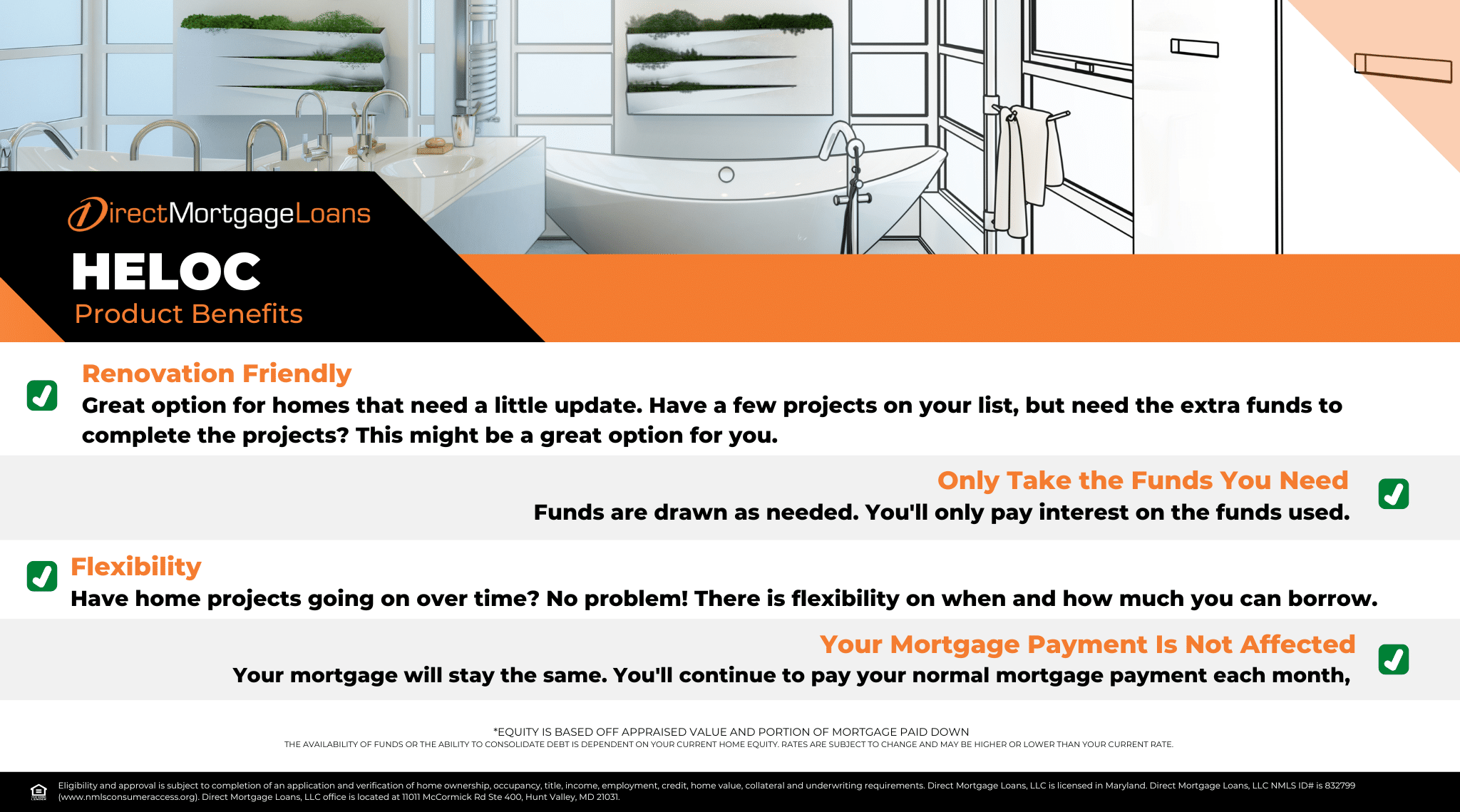

A Home Equity Line of Credit (HELOC) can be a good option, depending on your specific financial situation and goals. This type of loan can be beneficial in various scenarios, such as funding home improvements. For instance, it allows you to access funds for renovating or upgrading your home, potentially increasing its future return on investment.

If you’re struggling with high-interest debt such as credit cards, a HELOC could help you consolidate these various debtors into a single payment with a potentially lower interest rate, as the interest rates on credit cards are generally higher than mortgage rates. Additionally, a HELOC could serve as a financial safety net for unexpected expenses, like car repairs or medical bills. Additionally, for those looking to start a business, this loan could provide the initial capital needed to get it off the ground.

HELOC Loan Pros and Cons

If you are thinking about getting a home equity line of credit (HELOC), it’s important to weigh the pros and cons to help you decide if this option is right for you.

Pros of a HELOC Loan

- Flexible Access to Funds: Operates like a revolving line of credit, allowing you to access funds as needed during the draw period.

- Interest Payments Based on Usage: Only pay interest on the amount you borrow, not the entire approved sum.

Cons of a HELOC Loan

- Potential Debt Accumulation: Misusing a HELOC, by treating it like a credit card or other revolving credit account, could lead to accumulation of debt.

- Variable Interest Rates: Generally, HELOCs are associated with a variable interest rate, meaning your payment amounts can fluctuate.

HELOC Loan FAQ’s

Can you refinance a HELOC loan?

It is possible to refinance a home equity line of credit (HELOC). Specifically, you can either consolidate it with your first lien or take out a new HELOC or second lien to pay off the previous one.

Do you need an appraisal for a HELOC loan?

An appraisal is often required for a HELOC and it is an important step as it determines the home’s appraised value. This value is then used to calculate the amount of equity in your home, which in turn determines how much you could qualify for.

How much equity do you need for a HELOC loan?

The amount of equity needed for a HELOC varies by mortgage lender. However, most lenders prefer you to have at least 15% – 20% equity in your home. Typically, you can borrow up to 85% of your home’s value, minus your current mortgage debts.

Is HELOC interest tax deductible?

This will depend on specific scenarios. According to the IRS, between 2018 and 2025, interest on a HELOC used for home improvements is deductible. However, if used for personal expenses like credit card debt, it is not considered a deductible.

For tax years before 2018 and after 2025, interest may be deductible regardless of use. Consulting a tax professional is advised to clarify deductibility based on your specific situation.

Can you get a HELOC loan with bad credit?

While it could be more challenging, it’s not impossible to get a HELOC with a low credit score. Nevertheless, you will likely face higher interest rates and stricter qualification requirements. Building your credit score and reducing your debt-to-income ratio could improve your chances of approval.

What can you use a HELOC loan for?

A HELOC provides the flexibility to access and use funds as needed, allowing you to choose when and how much to borrow. Common uses include financing home renovations, creating a financial safety net for unexpected expenses, funding college tuition, large purchases, and vacations. Ultimately, the possibilities for use are up to you.

Can you use a HELOC loan for a down payment?

Using a HELOC for a down payment is possible, but it’s important to be aware that you will have to manage three monthly housing payments: your primary mortgage, the HELOC itself (for the borrowed amount used as a down payment), and the new mortgage on your second home. This can significantly increase your overall debt load.

Make sure to carefully assess your financial situation and ensure that your income can comfortably manage these additional payments over the long term. Keep in mind that missing payments on a HELOC, secured by your primary residence, could lead to foreclosure and the potential loss of both properties.

Do HELOCS have closing cost?

A HELOC typically does not have traditional closing costs like mortgage loans. However, there may be additional costs involved, such as borrower-paid appraisals or fees for accessing the line of credit.

Can I increase my HELOC loan limit?

In most cases, it’s unlikely you can increase your HELOC limit once it’s opened. It’s best to check with your lender to inquire about this possibility.

The availability of funds or the ability to consolidate debt is dependent on your current home equity. Rates are subject to change and may be higher or lower than your current rate. Eligibility and approval are subject to the completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral, and underwriting requirements. Direct Mortgage Loans, LLC NMLS ID# is 832799 (www.nmlsconsumeraccess.org). Direct Mortgage Loans, LLC office is located at 11011 McCormick Rd Suite 400 Hunt Valley, MD 21031. Equal housing lender.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.