When financial goals or unexpected expenses arise, homeowners often look to their largest asset—their home—to provide a solution. An FHA cash out refinance could be a powerful way to tap into your home’s equity, offering flexibility and financial security. This guide breaks down what you need to know, from eligibility and benefits to potential drawbacks.

Subscribe to our blog to receive notifications of posts that interest you!

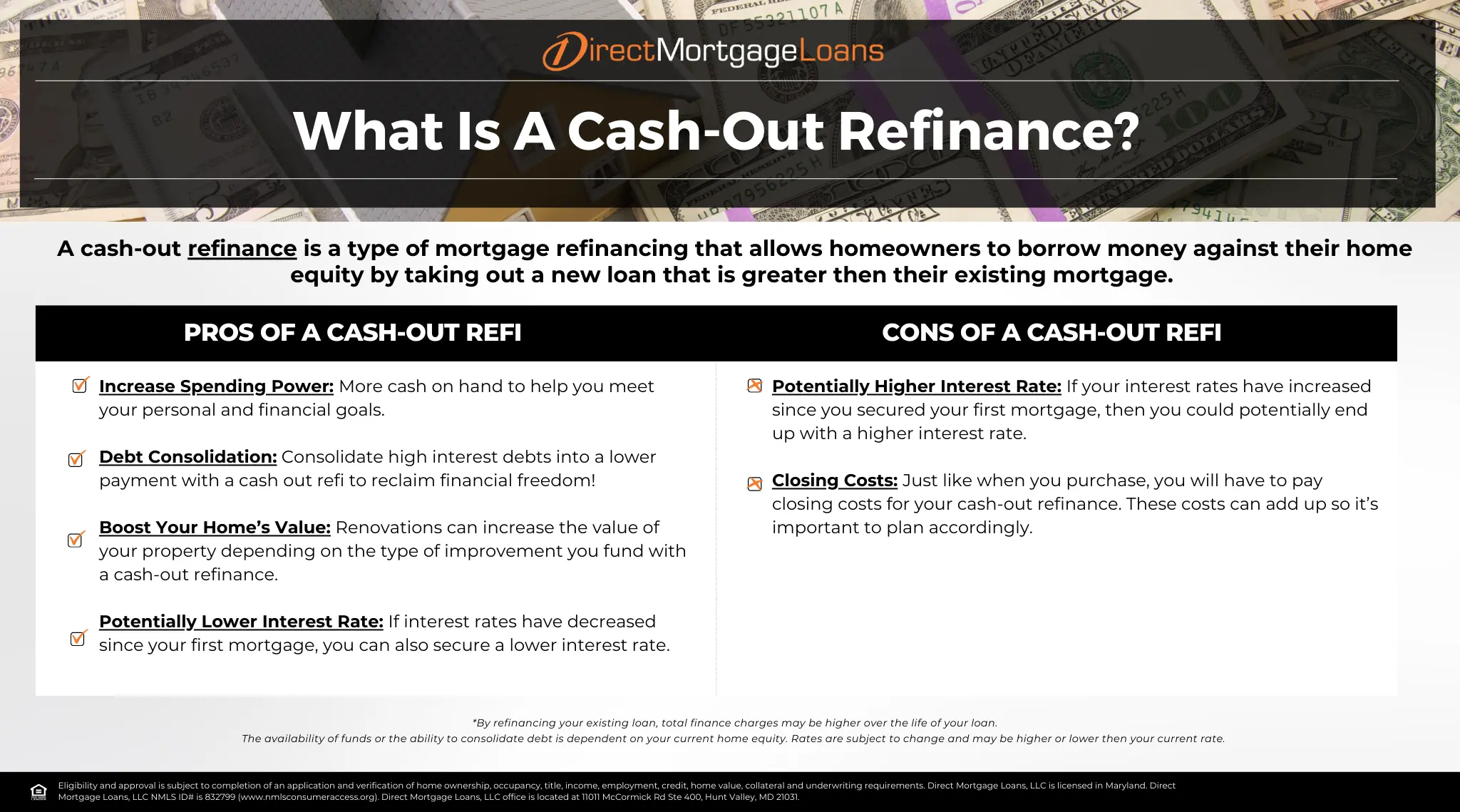

What is FHA cash out refinance?

An FHA cash out refinance allows you to replace your existing mortgage with a new one that is larger, giving you the ability to “cash out” the difference. This type of loan is insured by the Federal Housing Administration (FHA) and allows you to access the equity you’ve built up in your home. The funds can be used for a variety of needs, like home renovations, debt consolidation, educational expenses, or even starting a business.

Unlike standard refinancing, which focuses on lowering your rate or changing the terms of your loan, this option helps you convert equity into cash. The flexibility it offers is appealing to many homeowners, but it does come with specific requirements.

How much cash can you receive from an FHA cash out refinance?

The amount of cash you could access depends on your home’s value and the FHA’s lending limits. Typically, you could borrow up to 80% of your home’s appraised value. Here’s an example:

Imagine you owe $250,000 on a home valued at $500,000. With an FHA cash out refinance, you could borrow up to $400,000 (80% of the home’s value). After paying off the existing loan, you would have $150,000 available in cash, minus fees and closing costs.

How does FHA cash out refinance work?

- Application

Start by working with a lender such as Direct Mortgage Loans. Our loan officers will evaluate your financial and credit history to determine your eligibility. - Home Appraisal

An appraiser assesses your property to establish its current market value. This is essential for determining how much equity you can access. - Underwriting

During this stage, your mortgage lender reviews your documentation to ensure you meet all the requirements. This includes credit scores, debt-to-income ratios, and property eligibility. - Closing

Once approved, you’ll close on the new loan, paying off your old mortgage. You’ll receive the difference as cash, less any closing costs.

This process is similar to a traditional mortgage application but with the added benefit of cash out funds to support your financial goals.

FHA Cash Out Refi Example

Imagine your home is valued at $300,000, and your current mortgage balance is $200,000. This gives you $100,000 in home equity ($300,000 minus $200,000). If you choose to refinance with a new loan amount of $250,000, you would receive $50,000 in cash at closing ($250,000 minus the $200,000 balance on your existing mortgage).

With this option, your new mortgage would be $250,000, and the $50,000 cash out could be used to pay off other debts, make large purchases, or address other financial goals.

FHA Cash Out Refinance Eligibility Requirements

Considering a FHA cash out refinance could be a smart way to access the equity in your home for financial flexibility. However, there are specific eligibility criteria that you’ll need to meet to qualify. Here’s a detailed breakdown:

- Primary Residence: The property you plan to refinance must serve as your primary residence. This means that vacation homes, second properties, and rental properties are not eligible for FHA cash out refinancing. Moreover, to qualify, you must have owned and occupied the property as your principal residence for at least 12 months before the date of the case number assignment for the new loan.

- Exception: If you inherited the property, you could apply for a cash out refinance without needing to meet the 12-month occupancy requirement, provided that you have never used the property as an investment. If the property was rented out following inheritance, you must reside in it as your primary home for at least 12 months before qualifying for a cash out refinance.

- Credit Score: The FHA typically requires a minimum credit score of 580 for cash out refinancing; however, this does depend upon the lender’s discretion. A higher credit score may open the door to more competitive interest rates and terms, while a lower score could lead to higher costs. To maximize your benefits, it may be helpful to improve your credit score before applying.

- Loan-to-Value (LTV) Ratio: With an FHA cash out refinance, you could borrow up to 80% of your home’s appraised value. This LTV limit ensures that a portion of your home’s equity remains untouched as a buffer. For example, if your home is appraised at $400,000, you could refinance up to $320,000 (80% of $400,000). The new loan will pay off your existing mortgage, with the remaining amount available as cash at closing.

- Mortgage History: To demonstrate financial stability, you’ll need a history of on-time payments with your existing mortgage for at least 12 months. Missed or late payments could make it challenging to qualify or lead to less favorable loan terms. This requirement ensures that borrowers can manage their mortgage obligations consistently.

- Other Considerations: Mortgage lenders will also evaluate your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. It helps determine whether you can comfortably afford the new loan payments. While FHA guidelines generally allow higher DTI ratios than conventional loans, a lower DTI ratio could strengthen your application.

In addition to your DTI, lenders may assess your employment history, income stability, and cash reserves. Expect to provide documents such as pay stubs, tax returns, W-2 forms, and bank statements during the underwriting process. These steps help lenders confirm you have the financial means to support the new mortgage payments without undue stress.

These eligibility requirements are designed to ensure borrowers have the financial stability to manage their new loan terms.

FHA Cash Out Refinance Process

Here’s a step-by-step overview of the FHA cash out refinance process:

- Consultation and Pre-Approval

Connect with a lender like Direct Mortgage Loans to discuss your needs and see if you qualify for an FHA cash out refinance. - Document Collection

Be prepared to provide documents such as pay stubs, tax returns, credit information, and proof of homeownership. - Appraisal

An appraisal involves a licensed appraiser assessing your home’s market value through a detailed inspection and comparison with similar properties in your area. This appraisal helps determine the maximum equity you can access through your FHA cash out refinance and plays a key role in finalizing your loan amount. - Underwriting

Your lender reviews your application and supporting documents to ensure all FHA guidelines are met. - Approval and Closing

Once approved, you’ll sign the loan documents and access your cash out funds.

The process may take 30-45 days, depending on various factors like documentation and appraisals.

FHA Cash Out Refi vs Traditional Cash Out Refi

An FHA cash out refinance differs from a traditional cash out refinance in several ways:

Credit Requirements

FHA cash out refinances generally require lower credit scores, typically around 580, making them more accessible to borrowers with less-than-perfect credit. Traditional cash out refinances, on the other hand, often demand higher credit scores, usually in the mid-600s or above. This makes it slightly more difficult for those with lower credit scores.

Mortgage Insurance Premiums (MIP)

FHA cash out refinances require borrowers to pay both an upfront and an ongoing mortgage insurance premium (MIP). The upfront premium is typically 1.75% of the loan amount and can often be rolled into your loan balance, reducing the immediate out-of-pocket expense. This means if your new loan amount is $250,000, you would owe an upfront MIP of $4,375.

In addition to the upfront premium, there is also a monthly MIP payment that continues for the life of the loan. The exact amount of this ongoing premium depends on your loan-to-value (LTV) ratio and the term of your loan. These insurance premiums protect the lender in case you default, but they add to the overall cost of your loan.

By contrast, conventional cash out refinances typically only require private mortgage insurance (PMI) if your equity is less than 20%. Once you reach 20% equity in your home, you can eliminate the PMI, reducing your overall costs. This is a key distinction and can influence the total cost of the loan over time, making it a critical consideration when choosing between FHA and conventional options.

FHA Loan Limits

FHA loans have set maximum limits that vary by location and are based on the median home prices in a given area. These limits are typically lower than those for conventional loans. In areas with higher housing costs, the FHA’s loan limits could be more generous, but they still cap how much you could borrow, even if your home value or equity is higher. For example, in high-cost areas, the limit might be significantly higher than in regions with more moderate housing costs. However, it may still be restrictive compared to conventional options.

FHA loan limits are published annually and are adjusted to reflect changes in housing market conditions. Borrowers considering an FHA cash out refinance should check their local loan limits to ensure the desired amount can be obtained without exceeding FHA caps.

Conventional cash out refinances are subject to loan limits set by the Federal Housing Finance Agency (FHFA) for conforming loans. These limits are often higher than FHA limits and are adjusted annually based on changes in home prices. For high-cost areas, conventional loans also have high-balance or “super-conforming” loan limits, providing more borrowing flexibility for homeowners with significant equity.

Moreover, if your desired loan amount exceeds these conforming limits, you may be eligible for a jumbo loan, though these come with stricter credit and underwriting requirements.

A traditional refinance may be more beneficial if you have excellent credit and don’t want to pay mortgage insurance.

Pros And Cons of an FHA Cash Out Refinance

FHA Cash Out Refinance Pros

- Flexible Credit Requirements: Borrowers with credit scores as low as 580 may qualify, making this option accessible to a wider range of homeowners. This flexibility could be beneficial if you’ve faced past credit challenges but are now stable financially.

- Access to Equity: FHA cash out refinances allow you to borrow up to 80% of your home’s appraised value. This means you could tap into a significant portion of your home’s equity, providing ample funds for various needs such as home improvements, debt consolidation, educational expenses, or even major purchases. This level of access can offer the financial flexibility many homeowners need to achieve their goals.

- Flexible Use of Funds: Unlike some loan options that restrict how you use the proceeds, an FHA cash out refinance offers considerable flexibility. You could use the cash for virtually any purpose, from upgrading your home and investing in your property’s value. It can also be used to pay off high-interest debt, start a business, or cover unexpected expenses.

FHA Cash Out Refinance Cons

- Mortgage Insurance Premiums (MIP): FHA loans require both an upfront and an ongoing mortgage insurance premium (MIP). The upfront MIP is typically 1.75% of the loan amount, which could be added to the loan balance. You’ll also pay a monthly MIP for the life of the loan, which increases your overall costs. This is different from conventional loans, where private mortgage insurance (PMI) can be removed once you reach 20% equity.

- Higher Costs: While FHA cash out refinances offer flexibility, they often come with higher upfront costs due to required MIP and other closing expenses. This may offset some of the savings or cash benefits, especially for mortgage borrowers who plan to move or refinance again soon.

- Loan Limits: FHA loans have set limits based on location and median home prices, which may be lower than conventional loan limits. If you’re in an area with higher home values, this cap could restrict how much equity you can access. This makes it less advantageous compared to other refinancing options.

Other Options Besides an FHA Cash Out Refinance

Conventional Cash Out Refinance

A conventional cash out refinance lets you replace your current mortgage with a new one while accessing your home’s equity in cash. This option typically requires a higher credit score, usually in the mid-600s or above. However, it offers advantages like potentially lower interest rates. It also provides the ability to eliminate private mortgage insurance (PMI) if you have at least 20% equity. It is often preferred by borrowers with strong credit who want to avoid the ongoing mortgage insurance costs of FHA loans.

Home Equity Loan

A home equity loan provides a lump sum of cash that is secured by the equity in your home. This type of loan typically comes with the benefit of stable payments over the life of the loan. Unlike a cash out refinance, a home equity loan doesn’t replace your existing mortgage. It’s a second loan, which means you’ll have two separate payments to manage.

FHA Streamline Refinance

The FHA Streamline Refinance is a simple option for homeowners with an existing FHA loan who want to reduce their interest rate. It also allows them to change loan terms without an appraisal. It applies to primary homes, HUD-approved secondary residences, and rental properties. There are two types: credit qualifying, which reviews your credit and financial capacity, and non-credit qualifying, which skips these checks. To qualify, you must have made at least six payments on your current FHA loan and 210 days must have passed since closing. If you were in forbearance, you’ll need three consecutive on-time payments after completing your plan.

HELOC

A home equity line of credit (HELOC) works like a credit card that’s secured by the equity in your home. You could draw on the line of credit as needed during the “draw period,” typically 5 to 10 years, and pay interest only on the amount you use. Once the draw period ends, you enter the repayment period. During this time, you must pay back both the principal and interest.

Is an FHA cash out refinance right for you?

Choosing an FHA cash out refinance depends on your goals and financial situation. If you have built substantial equity and meet the requirements, this option offers flexibility. It also provides the opportunity to access cash when you need it most. Always weigh the costs and benefits before deciding.

FAQ’s About FHA Cash Out Refinancing

Can you use the cash from an FHA cash out refinance for anything?

Yes, you have the flexibility to use the cash for virtually any purpose. Whether you’re looking to make home improvements, consolidate high-interest debt, cover medical bills, invest in a business, or pay for educational expenses, the funds you receive from an FHA cash out refinance can help achieve your financial goals. The flexibility in usage of funds is one of the key benefits of this refinance option.

Is it possible to do an FHA cash out refinance if my current mortgage isn’t an FHA loan?

Yes, you could refinance into an FHA loan even if your existing mortgage is a conventional, VA, or another type of loan. This makes it a viable option for homeowners seeking more favorable terms. It also allows them to take advantage of the FHA’s flexible credit requirements while accessing their home equity.

What is the maximum cash out on an FHA loan?

Typically, you can access up to 80% of your home’s appraised value with an FHA cash out refinance. For example, if your home is valued at $400,000, you could borrow up to $320,000, including the amount needed to pay off your existing mortgage. This limit ensures that you retain some equity in your home as a safety buffer.

How long does the FHA cash out refinance process take?

The timeline for an FHA cash out refinance could vary but generally takes around 30 to 45 days from application to closing. The exact timeframe may depend on factors such as appraisal scheduling, document submission, lender processing times, and underwriting requirements. Working with an experienced lender could help streamline the process and minimize potential delays.

How much does an FHA cash out refinance cost?

The costs associated with an FHA cash out refinance typically include standard closing costs such as origination fees, appraisal fees, and title insurance. Additionally, you will be required to pay a mortgage insurance premium (MIP). This includes an upfront cost as well as ongoing monthly payments. The exact cost of these premiums varies, so it’s important to discuss the details with your lender to understand your specific financial obligations. Reviewing these costs ahead of time will ensure you have a clear picture of the total expenses involved in the refinance process.

What credit score do you need for a FHA cash out refinance?

The FHA generally requires a minimum credit score of 580 for cash out refinances. However, some lenders may have stricter standards based on their risk assessment. If your score is higher, you may benefit from better terms and interest rates. If your score is on the lower end, you may still qualify but could face higher costs or interest rates. Improving your credit before applying can help maximize your benefits.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.