Cash out refinancing and home equity loans are popular options for homeowners looking to leverage the value of their property. But what’s the difference, and how do you choose the right option for your needs? Let’s break it down.

Subscribe to our blog to receive notifications of posts that interest you!

Cash Out Refinance

Many homeowners opt for cash out refinancing to tap into the equity they’ve accumulated in their homes. Home equity acts like a built-in savings account which increases as your home’s value goes up. With this option, you could access the equity in your home by refinancing your existing mortgage and receive the remaining amount in cash.

What is a cash out refinance loan?

A cash out refinance loan allows you to access the equity in your home by replacing your current mortgage with a new, larger loan. The extra funds from the new loan are given to you in cash at closing. You could use this cash for different purposes such as consolidating debt, financing home renovations, or funding large purchases.

How does a cash out refinance work?

A cash out refinance works by replacing your current mortgage with a new loan for a higher amount. The difference between the new loan amount and your existing mortgage balance is given to you in cash. The amount of cash you can access is determined by your home equity, which is calculated by subtracting your outstanding mortgage balance from your home’s current appraised value.

For example, if your home is worth $300,000 and you owe $200,000 on your mortgage, you have $100,000 in equity.

If you complete a cash out refinance for $250,000, you will receive $50,000 in cash at closing. You would then have a new mortgage for $250,000 and could use the $50,000 cash to pay off debts or make other large purchases.

How much equity can you cash out of your house?

The amount you could receive from a cash out refinance will varies by lender and loan type, but the general rule of thumb is you must maintain at least 20% equity in your home. Most lenders allow you to borrow up to 80% of your home’s value, but it is best to only borrow as much as you need.

Utilizing Your Cash Out Refi Funds

There are no restrictions on how you can use the funds from a cash out refinance. Here are a few common ways you can utilize your funds:

- Lower Interest Rates: You might be able to lock in a lower interest rate than your current rate while pulling from your home’s equity.

- Home Improvement Projects: Many clients use cash out refinancing to renovate and make improvements to their homes.

- Debt Consolidation: Pay off your high-interest debt to get ahead of your finances and to consolidate your bills into one monthly payment.

- Tuition: If you or your child are considering higher education, then you could use the funds from your cash out refinance to manage the expense.

- Pad Your Savings: Want a larger emergency fund? Use your cash out to buffer your savings account.

- Investments: Use the funds you’ve earned to make financial investments toward your future.

When does cash out refinancing make sense?

When considering a cash out refinance, it’s important to ensure that it makes financial sense. For example, refinancing could be a good option if you can secure a lower interest rate on a new, larger loan, potentially resulting in long-term savings. Additionally, cash out refinancing is generally most beneficial for homeowners who plan to stay in their home for a longer time and have built up a significant amount of equity.

Home Equity Loan

A home equity loan could let you leverage the equity you’ve built up in your home to access cash. Essentially, your home’s value serves as collateral for the loan. If you’ve owned your home for a while and consistently made mortgage payments, you’ve likely accumulated equity that could be tapped into.

What is a home equity loan?

A home equity loan allows you to borrow against the equity in your home to address various financial needs. The loan amount is based on the difference between your home’s current market value and your remaining mortgage balance. You’ll get the loan as a lump sum, like a traditional mortgage, but repay it in fixed monthly installments over a predetermined term.

How does a home equity loan work?

A home equity loan is a separate loan from your current mortgage, allowing you to borrow against the equity in your home. Unlike a cash out refinance, a home equity loan does not replace your current mortgage.

Instead, it is a second mortgage with its own separate payment. Since a home equity loan is separate from your mortgage, none of the original mortgage terms will change. After the home equity loan closes, you will receive a lump-sum payment from your lender, which you will be expected to repay, usually at a fixed rate.

How do I get a home equity loan?

Direct Mortgage Loans offers a variety of mortgage options, including home equity loans. Keep in mind that you will need to meet specific requirements based on the type of loan and the lender you choose. Here is a general overview of the steps to obtain a home equity loan.

- Application: Submit an application with details about your home’s value and your financial situation.

- Approval: The lender appraises your home to determine your equity, and approves the loan amount based on the appraised value and your specific financial situation.

- Closing & Access to Funds: Once approved, you’ll finalize the loan details. After closing, you can access the funds needed during the draw period.

- Repayment: After everything is finalized, you’ll begin making monthly payments that cover both the principal (original loan amount) and interest on the home equity loan.

When A Home Equity Loan Makes Sense

A home equity loan could be a good option if you need a moderate sum of funds and prefer a fixed repayment schedule with predictable monthly payments. Home equity loans often have slightly higher interest rates than refinanced mortgages, but they could be easier and faster to obtain since they don’t involve replacing your existing mortgage. They are also a good option if you don’t plan on staying in your home for a long time, as you wouldn’t need to recoup the refinancing costs associated with a cash out refinance.

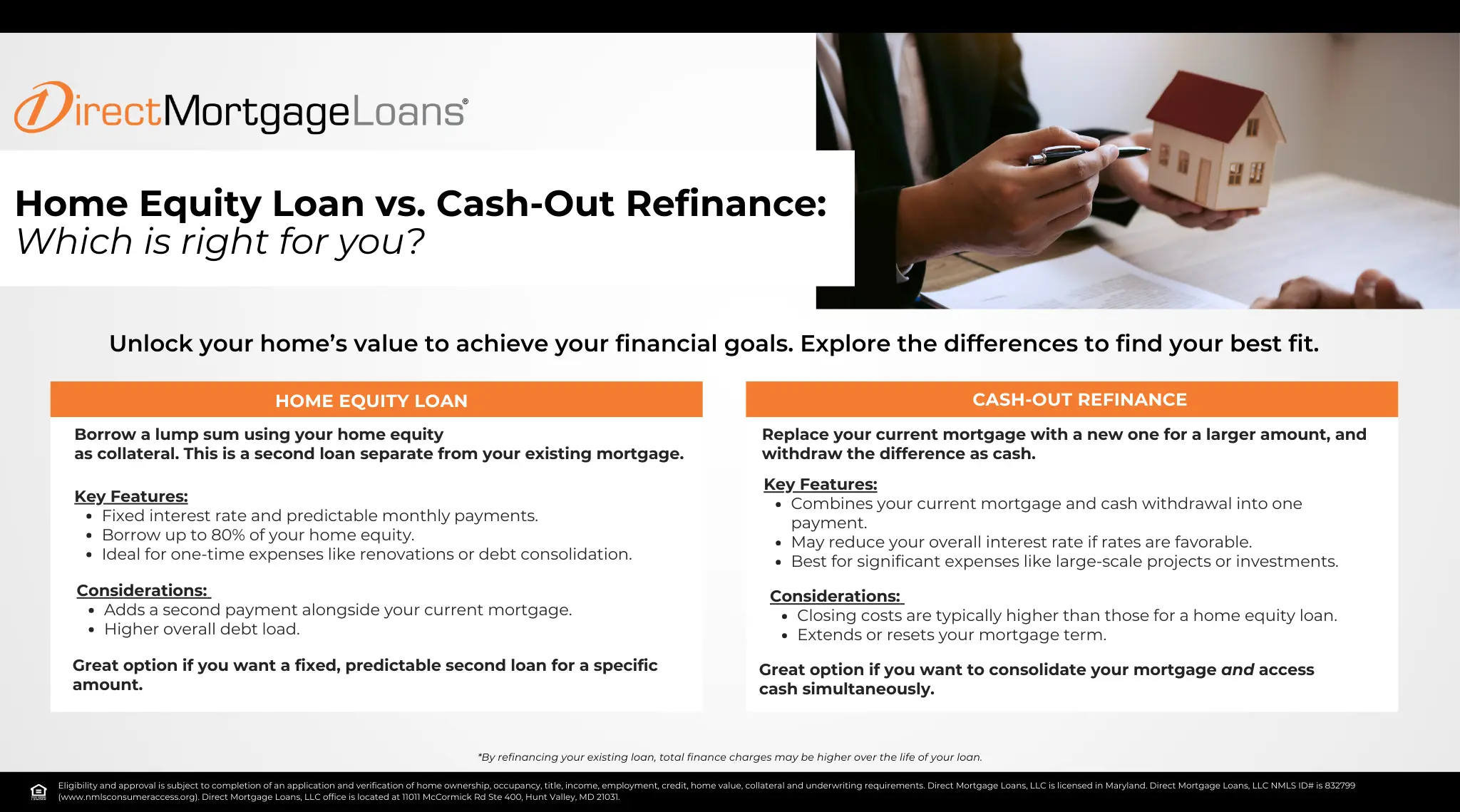

Cash Out Refinance vs Home Equity Loan

Choosing between a cash out refinance and a home equity loan depends on your financial goals and situation. Here’s a side-by-side comparison to help you decide:

| Criteria | Cash Out Refinance | Home Equity Loan |

|---|---|---|

| Primary Purpose | Replaces existing mortgage and provides access to cash. | Borrow against your home’s equity for a fixed sum. |

| Interest Rate | Generally lower than personal loans or credit cards. | Fixed interest rates |

| Tax Deductibility | Interest may be tax-deductible. | Interest may be tax-deductible |

| Impact on Existing Mortgage | Replace existing mortgage with a new one. | Creates a second mortgage with a separate payment. |

| Loan Structure | Single Loan | Second Mortgage |

| Repayment | Fixed Monthly payments | Fixed Monthly Payments |

| Term Options | Typically, 15 to 30 years. | Typically, 5 to 15 years. |

| Best Suited For | Long-term homeowners who want to lower their interest rate and access cash. | Homeowners looking for a fixed sum of cash for specific, short-term needs. |

Which is better a home equity loan or refinance?

When deciding between a home equity loan and a refinance, it’s important to consider your financial goals and circumstances. Both options allow you to access your home’s equity, but they function differently. Understanding the advantages and disadvantages of each can help you make an informed decision.

A home equity loan provides you a lump sum of cash. It’s great for one-time expenses like home improvements or consolidating high-interest debt. It’s a separate loan with its own interest rate and repayment terms, which are usually higher than your current mortgage rate.

A refinance replaces your current mortgage with a new one, potentially offering a lower interest rate. This could mean lower monthly payments or access to funds through a cash out refinance. However, remember that refinancing extends your loan term and might not be the best choice if you’re close to paying off your current mortgage. It’s recommended to speak with a Loan Officer who could assess your needs and recommend the best approach.

Cash Out Refinance vs Home Equity Loan FAQ’s

Can you pull equity out of your home without refinancing?

You could access the equity in your home without refinancing your current mortgage by using a home equity loan or a home equity line of credit (HELOC). Both options allow you to borrow against the equity in your home.

Is it hard to get a home equity loan?

Obtaining a home equity loan might involve stricter requirements compared to your original mortgage. Since you’re using your home as collateral for a second loan, lenders want to ensure you’re a reliable borrower. Several factors influence their decision, including your home’s equity, credit score, and debt-to-income ratio.

How much equity do you need to refinance?

When considering a cash out refinance, it is important to have at least 20% equity in your home. However, if you choose a rate/term refinance without cashing out, the equity requirement may be lower. For instance, if you are refinancing a conventional loan, you must have a minimum of 97% loan to value, while for FHA loans, the minimum requirement is 96.5%.

Is a home equity loan a mortgage?

A home equity loan and a mortgage serve different purposes. A mortgage is used to finance the purchase of a property, and it is repaid with interest over a longer period, usually 15 to 30 years. On the other hand, a home equity loan allows you to borrow against the equity in your home. You receive a lump sum of cash that you repay with interest over a fixed term, typically 5 to 15 years.

In simpler terms, a mortgage helps you buy a home, while a home equity loan lets you use the equity you’ve built up in your home to access funds for various purposes.

Can you refinance a home equity loan?

You have the option to refinance your existing home equity loan with a new one if you qualify for a lower interest rate or better loan term. Alternatively, you could refinance your home equity loan into a home equity line of credit (HELOC) for more flexibility in accessing your funds.

It’s best to speak with a Loan Officer about your specific situation and explore the refinancing options available to you. They can help you determine if refinancing your home equity loan makes sense for your financial goals.

Is a home equity loan a second mortgage?

Yes, a home equity loan is considered a second mortgage. Both types of loans use the equity in your property as collateral to secure the loan. The main difference lies in how you receive and repay the funds.

By refinancing your existing loan, total finance charges may be higher over the life of your loan. Eligibility and approval is subject to completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral and underwriting requirements. Direct Mortgage Loans, LLC NMLS ID# is 832799 (www.nmlsconsumeraccess.com). Direct Mortgage Loans, LLC office is located at 11011 McCormick Rd Ste 400, Hunt Valley, MD 21031.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.