How To Get A Vacation Home Loan

Owning a vacation property is a dream for many, offering a personal retreat and a way to build wealth through appreciation or rental income. Financing such a purchase, however, involves navigating different mortgage options, requirements, and strategies. This guide will walk you through how to finance a vacation home mortgage loan, so you can make an informed decision and turn your dream into reality.

Subscribe to our blog to receive notifications of posts that interest you!

Types of Vacation Home Mortgage Loans

When it comes to financing a vacation property, choosing the right type of mortgage loan is a critical step. Each loan type has distinct benefits and requirements, making it essential to match your financial goals and needs with the appropriate product. Whether you’re looking to purchase a cozy cabin, a beachfront retreat, or an investment property, understanding your loan options ensures a smoother path to ownership. Below we’ll explore some of the most common mortgage loans available for vacation homes and help you determine which might be the best fit for your dream property.

Conventional Loans

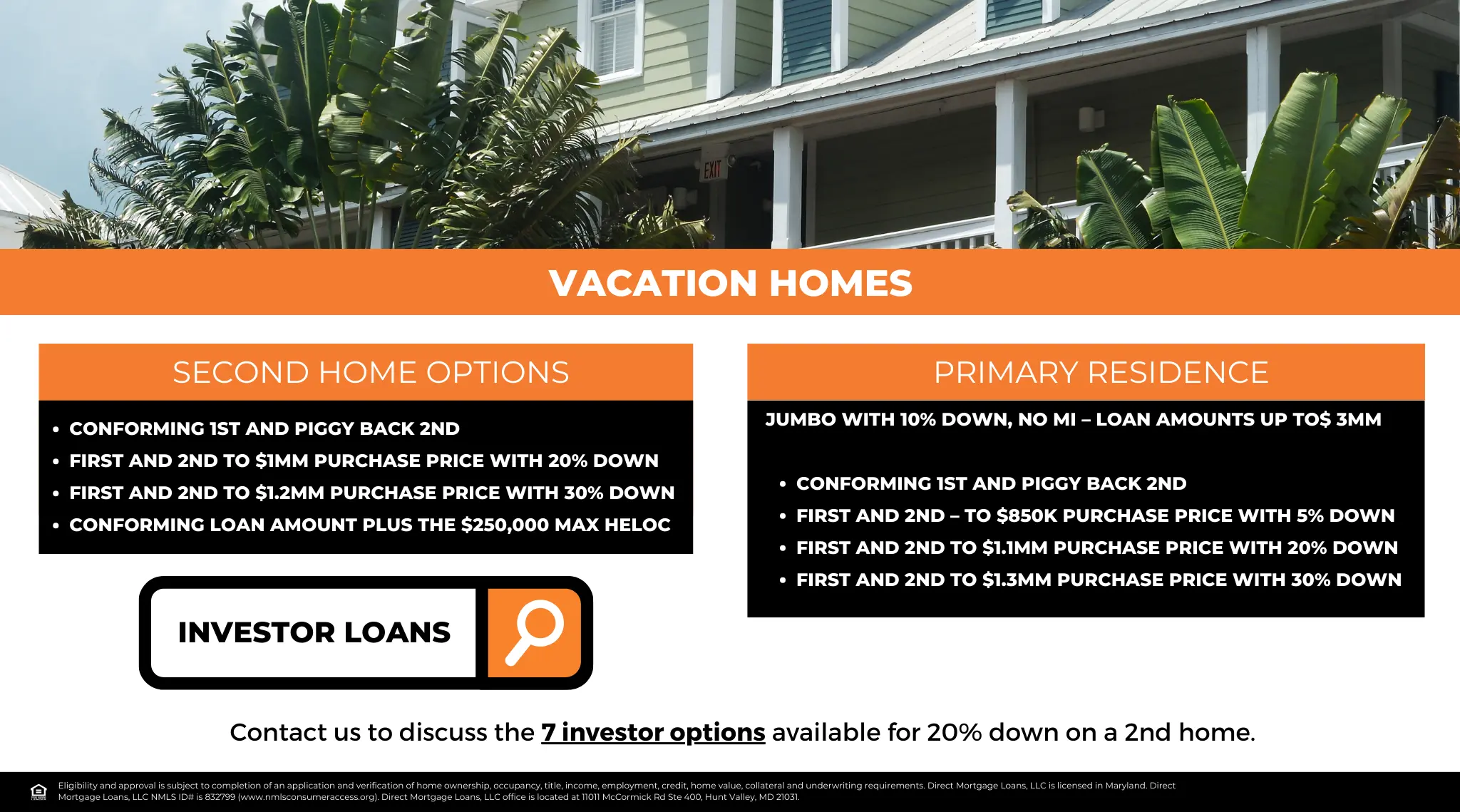

Conventional loans are among the most common ways to finance a vacation home. These loans typically require a 10-20% down payment, but terms vary based on your credit score and financial standing. Conventional loans offer flexibility for buyers with a strong financial profile.

Jumbo Loans

If your desired vacation home exceeds conforming loan limits, a jumbo loan may be necessary. Jumbo loans come with higher borrowing limits but often require more rigorous qualifying criteria, including a higher credit score and larger down payment. Direct Mortgage Loans offers options that make securing a jumbo loan manageable.

DSCR Loans

Debt Service Coverage Ratio (DSCR) loans cater primarily to investment properties, making them a potential fit if you plan to rent out your vacation home. These loans focus on your property’s rental income rather than your personal income, streamlining the mortgage qualification process for those with substantial rental income projections. Learning more about the pros and cons of DSCR Loans will allow you to have a better understanding of what loan type is right for you.

Note: DSCR loans apply only if the vacation home is truly a rental property.

Vacation Mortgage Loan Requirement

Qualifying for a vacation home mortgage comes with its own set of requirements, often more stringent than those for a primary residence. Because vacation homes are seen as higher-risk loans, mortgage lenders typically demand a strong financial profile from mortgage borrowers. Meeting these criteria is key to securing favorable loan terms and making your dream getaway a reality. Below, we will break down the main requirements for vacation home mortgages, including debt-to-income ratio, credit score expectations, and down payment guidelines, so you know what to expect as you move forward.

Debt To Income Ratio

Your DTI ratio, which measures your monthly debt payments against your income, is a key factor in qualifying for a vacation home loan. A lower DTI reflects a greater ability to manage additional debt. Direct Mortgage Loans has many resources which could help you assess your financial standing and provide options tailored to your profile.

Credit Score

Lenders look for a higher credit score when considering vacation home loans. Typically, a score of 700 or above improves your chances of securing favorable terms. A direct lender like Direct Mortgage Loans will work with clients to explore options that align with their financial history.

Down Payment

Vacation homes often require larger down payments than primary residences—usually at least 10-20%. The exact amount depends on your credit profile and loan type. Direct Mortgage Loans can guide you on the best ways to meet these requirements while keeping your financial goals in focus.

Vacation Home Mortgage Rates

Interest rates for vacation homes may vary based on your financial situation and market trends. Researching current market rates is essential but working with a Direct Mortgage Loans officer offers tailored guidance to lock in the best rate available. Personalized advice ensures you understand every option and optimize your loan terms.

How to Lock in the Best Interest Rate

To lock in the best interest rate, maintaining a high credit score, managing your debt, and locking rates during favorable market conditions are crucial strategies. Being financially stable opens the doors to more loan options and flexibility with payment, as well.

Financing Alternatives To Vacation Home Loans

Purchasing a vacation home doesn’t always mean taking out a traditional mortgage. There are several alternative financing options offering flexibility and potentially more favorable terms, depending on your financial situation. These alternatives could leverage your existing home equity, provide flexible credit lines, or tap into cash through refinancing. By understanding these loan options, you may find a creative solution that best fits your needs and helps make your vacation home dreams a reality. Below, we’ll explore home equity loans, HELOCs, and cash-out refinancing as potential pathways to owning your ideal getaway.

Home Equity Loan

Using your existing home’s equity could be a smart method to finance a vacation home. Home equity loans provide a lump sum for the purchase and come with fixed repayment terms. Consult with Direct Mortgage Loans to evaluate if leveraging your home’s equity aligns with your goals.

HELOC

A HELOC offers a flexible financing solution, acting as a revolving credit line secured by your home’s equity. It allows you to access funds as needed, making it ideal for buyers who want financial flexibility.

Cash Out Refinance

By refinancing your primary residence and taking cash out, you could access funds for a vacation home. This option may result in lower overall interest rates and could make financial sense for borrowers who want to maximize liquidity.

How To Apply For A Vacation Home Loan

Applying for a vacation home loan involves gathering essential documentation, such as proof of income, credit reports, and asset statements. Our team at Direct Mortgage Loans guides you through every step, ensuring a smooth application process tailored to your specific needs.

How can I find a vacation home loan lender near me?

Finding a reliable mortgage lender is crucial to your success. Direct Mortgage Loans provides personalized service to match your financial goals. Contact one of our expert loan officers to explore your options and find the perfect fit.

Vacation Home Mortgage Loan FAQ’S

Is it harder to get a mortgage for a vacation home?

Yes, obtaining a mortgage for a vacation home is generally more challenging compared to financing a primary residence. Mortgage lenders view vacation properties as higher-risk investments since borrowers are more likely to default on secondary loans during financial hardship. As a result, qualifying for a vacation home mortgage often requires a higher credit score, a larger down payment (usually 10-20% or more), and a lower debt-to-income (DTI) ratio. Direct Mortgage Loans specializes in helping clients navigate these requirements, ensuring you find the most suitable loan options for your vacation home goals.

Can I deduct interest on my vacation home loan?

In many cases, the interest paid on a vacation home mortgage loan may be tax-deductible, like the mortgage interest deduction for primary residences. However, there are conditions to consider. Generally, to qualify for the deduction, your vacation home must meet the IRS’s definition of a “qualified residence,” and there may be limitations based on how often you use the home personally versus how often it is rented out.

How many vacation home loans can you have?

The number of vacation home loans you could obtain largely depends on your overall financial profile, including your income, existing debt obligations, credit score, and the lender’s specific guidelines. In theory, you could own multiple vacation homes, each with its own loan, as long as you meet the lender’s requirements for additional mortgages. Direct Mortgage Loans can assess your unique situation and guide you through the process of securing financing for multiple properties, offering personalized advice tailored to your investment goals.

Can a VA loan be used for a vacation home?

No, VA loans are exclusively intended for primary residences and cannot be used to purchase a vacation home. VA financing is designed to help eligible veterans, service members, and certain military spouses buy or refinance their primary residence, offering benefits like zero-down financing and competitive interest rates.

Is a vacation home considered investment property?

The classification of a vacation home as an investment property depends on its use. If you primarily use the property as a personal retreat with only occasional rentals, it is typically considered a second home. However, if you rent out the property regularly, or treat it as a source of income, it may be classified as an investment property. This classification impacts your mortgage terms, interest rates, and tax treatment.

What is the difference between a vacation home and a second home?

While the terms “vacation home” and “second home” are sometimes used interchangeably, there are key differences. A vacation home is often used for short-term stays and may be rented out when not in use. A second home, on the other hand, typically serves as a part-time residence and is not rented out to others. These distinctions can influence your loan terms, tax treatment, and how lenders assess risk.

Are mortgage rates different for vacation homes?

Yes, mortgage rates for vacation homes are often higher than those for primary residences. This is because vacation homes carry more risk for lenders; borrowers may prioritize payments for their primary home during financial difficulties, increasing default risks for secondary properties. However, your specific rate depends on factors like your credit score, down payment amount, and overall financial health. Working with Direct Mortgage Loans ensures you receive personalized rate options tailored to your financial goals, helping you secure competitive terms.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.